The longer interest rates stay at zero, the longer this assumption gets baked into the structure of the economy and the more chaos that'll be unleashed when and if they finally go up. There were no interest rate hikes between 2006 and 2015, and interest rates have been at zero for 8 out of the last 13 years.

It's easy to blame COVID for the latest rate cut, but interest rates were already dropping in late 2019. The Fed slashed rates 3 times from July-December, and then went straight to zero in March. I've heard (from finance industry professionals) that the reason was that corporate debt loads rapidly become unsustainable when interest rates go up. They need to roll their debt when it comes due, but debt levels are now such that they rapidly become insolvent when borrowing costs rise.

I'm seeing more people reach the obvious conclusion that interest rates are simply not going to rise. The Fed has an incentive to keep them low - they'll get mass bankruptcy and mass unemployment otherwise, contrary to their full-employment mandate. The government has an incentive to keep them low, since it keeps borrowing costs on the rapidly-ballooning federal debt low. Retirees have an incentive to keep them low, feeding 401K bubbles that they need to live on. Young adults have an incentive to keep them low: it keeps student loan and car payments manageable, and inflation reduces the real value of their debt. Homeowners have an incentive to keep them low: the value of their home will drop if mortgage rates go up. The only people with an incentive to see them go up are vulture funds & shorts, who nobody likes anyway, and prospective homeowners, who are largely the same people with loads of student loan debt that they'd like to see inflated away.

If everybody has an incentive for rates to stay low, they will stay low. This ends in hyperinflation.

Or it ends in a market crash. When interest rates are zero, savers have no choice to build on wealth except the market. This is why the market continues to hit higher and higher records, and at some point people will lose trust in the market and flee.

Hyperinflation can always come after the bubble bursts.

Is there anything wrong with using markets to store value? Must we also have government bonds to store value? If you're in a diversified US index fund, it's basically a bet that the US will continue to do well. If it doesn't, you have bigger problems than the financial.

the primary purpose of a market is supposed to be to accurately allocate productive resources and pick winners and losers. In a market constantly flush with cash where everyone just buys index funds that discriminatory function basically vanishes and you have a political commitment to always make the stonks go up even if it supports zombie firms. Which is already the case tbh.

Same with housing. Nimbyism is such a big deal in the US because rather than seeing housing as a utility that should be cheap, it's become a store of value that must always go up.

There's a growing movement to get away from index funds. This year, tech stocks have exploded. ARK Invest has vastly outperformed the S&P 500 and Nasdaq-100. Ultra-low interest rates tend to have people going for increasingly high-risk, speculative investments, such as tech companies. The bolder and more futuristic the vision, the better. Obviously, this could end badly as well, but, people are starting to pick individual stocks instead of index funds.

The problem is knowing when to enter and exit the sector-specific funds. It might beat the S&P in a trailing 12 month window, but it's unlikely to do so over a 5 or 10 year window.

It will definitely end badly. I guess it’s driven by desperation for returns. Diversification is a risk reduction strategy as old as the Bible; stock picking is not about preserving wealth or growing wealth, it’s about bootstrapping it.

There is absolutely nothing wrong with using paper markets to store value.

The problem appears when valuation are caused only by the "store of value" usage, because it has no anchor on the real world, and thus, can vary freely from 0 to infinity.

There’s nothing wrong with storing your possessions in your car; it’s just not what it was designed for and your possessions are at greater risk of theft.

Similarly, if you need a risk-free value store (e.g. because you’re very close to retirement) the market is not going to provide that for you.

That and real estate prices. People borrow insane amounts of money right now because they can due to the ridiculously low (in some places negative!) interest rates. Once those go up to reasonable levels (say, 5...10 % annually) suddenly they won't be able to pay for their house anymore and it's 2008 all over again.

When getting a mortgage, at least on my side of the pond, you get the option to fix the interest. I've set mine to 30 years fixed (the duration of the mortgage), because a few years ago it already seemed like the rates were bottoming out. I was wrong, but I don't regret fixing my mortgage interest rate.

A more pressing matter is that people are no longer able to afford a house, especially if they're young / early in their career.

I bought a home in 1998 with a variable-rate mortgage.

The interest rate was 7.5% and my friends told me I was foolish not to pay 9.0% for a 30-year fixed rate mortgage. They calculated nightmare scenarios if rates doubled or tripled while theirs held constant.

Every year since then, my interest rate reset downward until it hit the lower limit of 2%. Even though my required payment decreased, I kept paying the original payment amount and paid off the loan 10 years early.

My friends paid hundreds of thousands in additional interest over the years for the peace of mind of a fixed rate.

PSA: 2021 to 2031 might be different than 1998 to 2018.

Yes, but you can always refinance a fixed rate mortgage into a new fixed rate mortgage at a lower rate. You have to do it intentionally, and it’s optional, so you only do it when the rate moves in your favor. Variable rate mortgages change automatically, which means they can move against you.

That was then. Today you can get a fixed rate in the high 2% range. If rates rise as expected, it will be those who chose the fixed rates who will be OK, and those who chose variable will be screwed.

Where do you live that you can fix a mortgage rate for 30 years? This is impossible (or at least, highly rare) in Australia (you can get a fixed rate but only for up to ~5 years).

In the USA it’s pretty standard. The 30 year fixed rate mortgage is probably the most popular by far. And then you refinance it over time as rates fall.

Adjustable rate mortgages exist too but got a lot of people in trouble in 2008. I think a lot of them are only allowed to adjust by a certain percentage regardless of interest rates each year they’re eligible to.

It also keeps the minimum payment lowish - I went for a 30-year fixed, refinanced it once when rates went crazy low, and paid roughly double what I needed to (apart from months when I couldn’t). It paid off in ~13 years. I could have got a 15-year fixed on slightly lower rates, but the flexibility was worth the rate delta for me.

For down payments <20% mortgage insurance is needed (usually from the federal government subsidiary, like Fannie/Freddie), but not for larger down payments: that's all free market.

A fixed rate is just a derivative product (an Interest Rate Swap) attached to the mortgage, and people are happy to buy and sell them, why would you say it would not exist in a free market?

Case in point: there is no such government policy in Spain, yet most banks happily offer fixed rates.

You just need to hedge the fixed mortgage you are selling and add some interest to make profit.

In the USA it's apparently common, but seems unusual everywhere else. In the UK, 5 years is the maximum and 2 years is more common. People rely on rolling over the mortgage to a new fixed-rate offer, but that can be problematic as it's not guaranteed that good offers will be available after the fixed term, and as many found out in 2009, it's not guaranteed that fixed rate mortgages will be available at all. Also it costs a ton of money and time to roll over the mortgage because you're essentially buying the house all over again.

"In the USA it's apparently common, but seems unusual everywhere else."

It's not just common in the US, it is the de facto standard across almost all mortgage types and sizes. Even weird, non-conforming properties with "jumbo" sized loans can get fixed at 30 years.

Also, I will point out that in both Switzerland and the Nordic Countries, 40 and 50 year mortgages are now in very common use:

"Repayment periods in Switzerland can be incredibly long, with deals lasting between 50 and 100 years being relatively common."[1]

"Swedish regulators calculated in 2013 that the average mortgage term was around 140 years."[2]

In fact, now that I think about it, I am surprised that the US culture of "financial innovation" has not produced more standardized long-duration mortgages ... I do not know anyone, for instance, with a 40-year term ...

You can get 10-year fixed in the UK {1], and even that limit is surprising to me. I thought 20-year fixed was available (pretty sure it used to be) but apparently no more...

Since 2008, from everything I've seen lenders are much more restrained about creditworthiness, so there are probably far fewer people buying houses that are only marginally affordable initially, with variable rates, and an interest-only initial period or other pre-programmed increase in basic payments. So I don't think the risk of that kind is as great as going into 2008.

But, yes, buying with variable rate mortgages when interest is at historic lows rather than paying a little bit extra initially for fixed rates is risky, and on a society wide scale that risk is going to materialize at some level.

The majority of Americans do not have any real (or any at all) amounts of money invested in the market. That may change slowly as more people come online, but right now the majority of the stock is owned by a small percentage of the workers of the country. I'd expect there to be a very long road ahead of us before we find most Americans holding a sizable amount of their capital in the market or even in a bank account at all.

"Just a modest majority of Americans, some 55%, own stocks, according to an April 2020 poll by Gallup, which asks whether households owned stocks either directly or as part of a fund."

33% * %42 = ~14%. And while the number is debatable, depending on how we define "significant", only a portion of that 14% has significant wealth invested in the stock market.

I agree with the previous poster. The vast majority of Americans (including employed Americans) aren't invested in the stock market in any meaningful way.

The same applies to cash once a critical mass of people believe there's an effectively unlimited amount of it flooding the market. That's what hyperinflation is. You really don't want to be in cash if that happens.

See the performance of Venezuela's stock market over the last 5 years:

(The "crash" in late 2018 was the redenomination of the bolivar at a 1:1000 ratio, which affected everything denominated in bolivars, including the stock market.)

My grandfather bought a mansion in SF (Dolores St) for $8K in 1934 (approx). You can optimize for a 1929-style crash (hold cash), and you can even plan for hyperinflation (anything but cash), so the trick is to figure out which way to go.

I think that's the appeal of Bitcoin and/or Gold: it's both cash in that it might act as a safe haven in the case of an asset crash and would retain it's value during hyperinflation (since you can't print more of it).

Though bitcoin has really been untested as a safe asset and currently behaves more like a speculative one.

I think Bitcoin has huge potential right now, even after its recent run up. It could easily 4x to 6x from here, before the next halving. It could also drop by half, but at least the rewards are asymmetric with the risks.

But even though I'm optimistic about Bitcoin, I don't see it as crash-proof except in one crash scenario. It's mostly a speculative risk-on asset that loses value in crisis scenarios. We saw that in the covid crash in March last year as Bitcoin prices tumbled along with other markets.

The one crash scenario where Bitcoin doesn't crash is if Bitcoin is the thing that triggers a crisis of confidence in fiat assets. That's the hyperbitcoinization scenario that still looks improbable, but easier to imagine now than it was a couple years ago.

Gold has been confiscated by FDR. Bitcoin clamp down is coming: we have recently learned from Yellen that it's primarily a terrorist tool, and that it also causes global warming.

It would be interesting to see how much the gold mining industry contributes to global warming (including not just extraction, but processing and shipping). Trading, too, but I suppose that's done mostly by contract, and not shipping gold bars around...

People are giving too much credit to cryptocurrencies as the only vehicle for dodging inflation. Any asset that rises with inflation (most of them) is a sufficient vehicle for avoiding having your cash devalued.

People could simply exchange their domestic currencies for foreign currencies of more stable countries. That's what happens in countries with hyperinflation right now, despite access to cryptocurrency.

The only real advantage of cryptocurrency is that it could be transferred around hypothetical government controls. That's more of an extreme edge case scenario, though.

To be clear: The US inflation is too high, IMO, but it's nowhere near hyperinflation or government collapse. The average citizen is more likely to benefit from recent stimulus packages than to lose out from it. It's not like everyone keeps their 401K invested in pure cash.

That said, we're overdue for interest rates to start creeping up. COVID is coming to an end quickly and the unemployment never really got out of control in the first place. People aren't going to go bankrupt if their mortgages go back to 4-5% instead of 2-3%

> People could simply exchange their domestic currencies for foreign currencies of more stable countries

Most of the developed nations are competitively devaluing their currencies. If one country does it, they gain a trade advantage: their exports are relatively cheaper on the world market, so consumption flows to their industries and makes them wealthy. Therefore once one country does it, they all have to do it, lest all their export industries become uncompetitive and they lose those jobs.

I've heard some speculation (nicely backed up by data [1]) that the real reason we couldn't follow through with monetary tightening 2015-2018 is because it created a carry trade of investors borrowing in Euros and investing in dollars [2], which led to a continual outflow of dollars out the door.

If hyperinflation hits it will likely hit nearly all the developed world in short succession. If the dollar goes, all investors are going to dump dollars for Euros, but if they do that the value of the Euro will skyrocket, which means European exports will become super expensive and Euro-denominated debt will be harder to pay off, which will spur European central banks to dump more Euros into the system. As long as we have free capital flows there's no way around this: inflation in one fiat currency will lead to inflation in others. That's why people are looking for non-fiat currencies. (You're right that tradable assets like stocks can fulfill this job rather than cryptocurrency, though.)

> As long as we have free capital flows there's no way around this

I think that's the gist of it, and as such I also think that free capital flows will be massively restrained in the scenario you mention (a scenario which I also find very likely).

A similar thing has just happened with the freedom of movement for people, a "right" that the great majority of us had taken for granted, and then Covid came and that "right" was forgotten about like it never had existed.

The ECB is a lot more politically constrained than other central banks. It doesn't have a single master but is beholden to various degrees to the member states of the EU and especially Germany which is utterly paranoid about currency devaluation.

Don't forget the ECB raised rates during the onset of the financial crisis circa 2007-8 when everyone else was cutting desperately because of their inflation targetting mandate.

Buying Bitcoin to hedge inflation instead of just buying TIPS is like saying: I think the price of AAPL will go down, so I'm going to get some lottery tickets.

And you would be wrong. Inflation != asset prices. Don't make me post the global savings glut thing again... Also "rigged" is just conspiracy language. YOU CAN LITERALLY LOOK UP THE INDEX YOURSELF. Channel your inner hacker and do it, learn something, you don't need anyone's permission. I'll even help.[1]

I'll give you the "Angry" part, but you're going to have to work harder to convince me of "Skillzz." I can imagine a thousand ways to "rig" an inflation index to rationalize money printing. A couple years of latency here, a trimmed mean over there to exclude assets, bingo bango mission accomplished. Money printer goes brrrrr!

I actually have spent considerable time poking through the basket definitions and while I was generally impressed by the effort I saw, the extreme sensitivity to minutiae and extreme incentives to obtain a particular conclusion make me hesitate to bet my portfolio on its integrity. I haven't re-implemented their entire methodology in an economic model and run monte-carlo simulations to evaluate their competence in the face of obvious hypotheticals but I'm pretty sure you haven't either. By comparison, "bet on assets to hedge inflation" requires much less concentrated faith in the continued wellbeing of a convenient scapegoat.

From a programmer's perspective, you are right that there are no technical barriers to constructing an arbitrary index that delivers whatever value of inflation you want. But of course that is the case for most human things. Which is why institutions are important - hopefully while we are over here being honest and thinking hard about programming, there are people over there being honest and thinking hard about the consumption basket. But then a lot of us work in adtech so maybe that honesty is questionable...

And then there are the other even more severely complicated parts. If next year's iPhone is better but costs the same amount, that's deflation. You got more for the same amount of money. How do we quantify that? Those are called hedonic improvements. How do you account for free services? What is Google worth? What if a new thing comes out that has never existed before? How do you compare that to the previous consumption basket? It would be relatively easy to argue that the preponderance of brand-new, incomparable, improving every year, cheap/free tech stuff that we are living in a relatively deflationary environment. You get more, better stuff every year for less money!

Hedonic improvements like the ones used to multiply up Intel's revenue in order to claim that "US manufacturing is doing better than ever!" while we were shipping our entire industrial infrastructure to China?

I found that episode informative and convincing, but in the exact opposite direction. I stuck my neck out on the basis of those numbers while arguing with conservative family members and it turns out the numbers were rigged after all. For a very reasonable definition of rigged.

In the face of shenanigans, I tend to put more faith in simple concepts like "assets hedge inflation" than in indices.

I'll take the other side of that argument. It's an interesting article! But it doesn't make me think that the numbers are "rigged," just that they have been misinterpreted. Semiconductors are getting way better, and have been for a few decades, and that counts as an awesome productivity improvement in manufacturing. If you just look at the top-line number, it says "manufacturing is getting more productive," which in an aggregate sense is still true! But it seems a lot of people though that meant "manufacturing is getting more productive because we have a lot of robots" even though manufacturing employment is declining, rather than "manufacturing is getting more productive because our semiconductor fabs are awesome and the rest of the sector is bleeding out." Which is what it actually meant.

The "US manufacturing is super productive" narrative is unfortunate, especially if policymakers were making decisions based on it. But it doesn't really call into question the data or methodology, just that people have misinterpreted it. But the people who are actual experts in this area are writing papers about that! This paper is from 2014[1], and she's been writing about this since 2010! With economists from the Federal Reserve system, no less.

edit: I guess my point is, the point that article makes isn't, "the game is rigged, inflation is made up, we should use shells for currency." The point it makes is, "don't just read the top-line number and then write an opinion article, make sure you read the breakdown first."

Also, assets do hedge inflation. Most of them, anyway. I never argued otherwise. Just that asset price increases are not the same thing as inflation.

I'll grant you that it's entirely possible for this sequence of events to have happened spontaneously, without any malice, on the basis of misunderstandings. It could also have happened through the selective promotion of convenient metrics (which I'd argue does constitute rigging, just by a different party), or indeed through actual malice, though I tend to share your doubts on that front.

My invocation of the term "rigged" was not charitable but that's pretty far from saying it was actually incorrect. If I had to bet, I would bet on the middle possibility: metrics are built honestly but selectively promoted in accordance with political agendas in a manner that I would be comfortable to characterize as "rigged."

In any case, assigning blame is one thing and designing portfolios robust to this kind of mishap is another. Fortunately, the difficult parts of assigning blame are completely irrelevant to portfolio design. No matter who was responsible, the correct response is to avoid metrics that are easy to misunderstand (or rig!). Which brings us right back to favoring "assets hedge inflation" over "TIPS hedge inflation."

> Also "rigged" is just conspiracy language. YOU CAN LITERALLY LOOK UP THE INDEX YOURSELF.

The idea that the government inflation indexes are rigged is conspiracy language. They are talking as if people from conservative think tanks and corporate boards are having the government fix inflation indexes to their way of thinking, or even retroactively setting inflation indexes to their way of thinking ( https://en.m.wikipedia.org/wiki/Boskin_Commission ).

They probably will, but central government authority tends to collapse when hyperinflation begins. Venezuela (and the international community recognizing Venezuela) can't even agree on who the president is, and 60% of the Venezuelans who do work do so in the informal sector.

Remember Crypto knows no borders, it's decentralized, peer to peer, and private keys aren't seizable by force. Central banks may outlaw it, and that will hurt, but it's not going to put an end to it. Especially should USD go into hyperinflation and all hell breaks lose.

1. Central banks (at least, the US Fed) doesn't have the authority to declare crypto tokens illegal unilaterally.

2. EO 6102 made sense with the gold standard. It wasn't just an "FU" to gold hoarders, but a way to raise revenue to counter the depression. It's not clear to me that it would make sense for such a confiscation of crypto, especially if the legislature were to try option #1.

> Central banks will outlaw it because they can't control it and devalue it

Except that, many rich investors and large corporations are putting money into crypto as we speak. Some of those large investors may include people who work in the government and at central banks. I tend to think that, these people will have a conflict of interest there. It might be in their own best personal interest to not ban crypto, and to leave that door open. In other words, it might soon be too late to ban crypto. The ball already started rolling down the hill.

> In other words, it might soon be too late to ban crypto. The ball already started rolling down the hill. In other words, it might soon be too late to ban crypto. The ball already started rolling down the hill.

Great analysis. Give it another few years: then when most of the S&P companies will hold crypto, along with your richest supporters and voters, trying to ban it will become political suicide.

Virtually any investment, other than cash or a money market account.

Assets, stocks, real estate, all of the things that inflate with inflation. Crypto gets a lot of undue attention as a way to escape inflation, but investors have been investing in assets to losing buying power long before crypto came along.

Or the dollar could just hyperinflate, which would end the market bubble. In which case the market bubble will never burst, as denominated in USD. Look at Venezuela's IBVC.

Hyperinflation of the dollar will be nothing like Venezuela. The dollar is the reserve currency in many nations, and the primary currency for oil. If we hyperinflate the entire global economic system will be impacted.

>When the one year treasury yield gets back above 2%, we are leaving the easy money era.

zero percent and negative interest are like a roach motel for investors in 2021. no ones leaving anything.

in 2008 the fed introduced quantitative easing and by 2020 they'd never left it. the fed just..."decided" that they didnt want stocks to crash, ever, and increased the amount of liquidity in the market without thinking twice.

in 2010 they tried to ween the market off QE and were rewarded with an 800 point tantrum plunge. now its 2021, the feds 1993 crisis to real earnings (cheap credit) is now de-facto how most of American society runs. their 2008 stop-gap (QE) cannot be undone without a massive economic depression and every day hyperinflation looms on the horizon.

This means there is also no possibility of a minimum wage increase (doubling to $15)...ever, as no one knows if it would be good enough to trigger a collapse or not.

despite the furious protest of real-estate moguls many people see housing as a bubble, and when it pops, QE will not solve the problem a second time around.

The US has a bunch of real resources. They are being directed to companies that are basically burning them for no reason ($X off resource in, $X less a bit out).

If they demand that companies show any sort of ability to generate more than they consume, then too many companies fail. So instead they are encouraging wasteful companies to keep on doing what they do.

At some point, the deadweight builds up and a series of worsening crisises emerge as people start fighting over what is left, which is no longer enough to have a peaceful society.

The problem is that if losers don't lose, they will end up in control of the economy. I could out-compete almost anyone on vast amounts of borrowed money while making a loss.

Companies like Uber "burning" money is a wealth transfer from Uber investors to Uber customers, employees, and vendors, creating tremendous value where there was once none (labor exploitation notwithstanding).

Is it sustainable? No. But I disagree that it represents waste from anyone's perspective but the shareholders'.

The value creation I had in mind was with respect to the people who were previously very badly underserved by the traditional taxi/black-car industry, and are now served by Uber.

> The longer interest rates stay at zero, the longer this assumption gets baked into the structure of the economy and the more chaos that'll be unleashed when and if they finally go up.

[…]

> If everybody has an incentive for rates to stay low, they will stay low. This ends in hyperinflation.

But even that's subjective. If home ownership were considered essential, we'd say there's high inflation. The only unquestionably high inflation is Weimar-style. Everything in the middle is justifiable in either direction, and gray matters seem subject to whichever ways the political winds blow. If it's convenient for rates to stay low, they will.

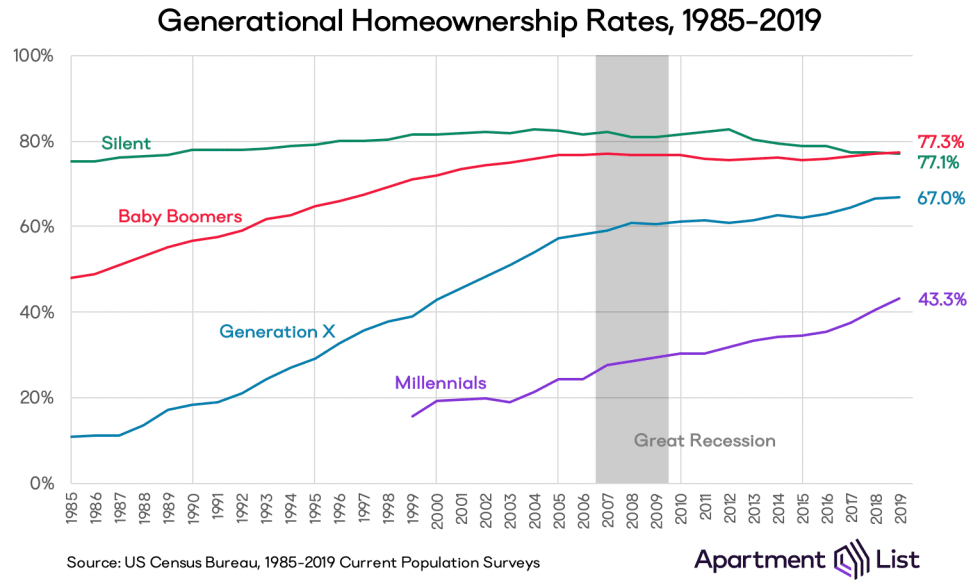

Correct, and housing services do not mean ownership. Inflation metrics say a 700 square foot econobox is the appropriate measure of cost. If you continually shift the basket, then you can craft whatever CPI number you're looking to achieve. And ownership levels by generation aren't what they used to be:

Sure. But that's not inflation. That's an increase in housing prices. If housing prices rise but rents do not, it doesn't make a difference to consumption - your consumption is either the rent you pay or the imputed rent. If buyers want to bid up the price of housing past what renting it out will pay for, that's their problem.

And at the risk of just reposting this comment on HN all the time. Focusing on central banks as the driver of asset price increases is looking in entirely the wrong direction. There is a third component that pushes both asset prices and central bank policy - the global supply/demand of savings vs investment opportunities. Which is driven mostly by demographics. China's massive working class, and the unprecedented rate at which they are getting wealthier, and their savings rate which is like >10x the average US citizen means there is a huge increase in the global supply of savings. Which bids up asset prices and pushes down yields, as savers compete with each other to buy up the extant profitable and safe opportunities. Central banks are the on the receiving end of this too: over-saving pushes down the natural rate of interest, which means policy rates must be lower to respond (unless you want to condemn some working Americans to unemployment). So long-term interest rates fall, and central banks have less operating space to smooth out the business cycle by moving short-term rates.

The U.S. Bureau of Labor Statistics reports (10-Feb-2021) that the Consumer Price Index (all items index) increased 1.4 percent over the last 12 months.

That's not "nearly everything". Most people don't spend their salaries on lumber or copper. If anything, it shows how little the prices of raw commodities affect consumer prices.

It's also hardly evidence for impending hyperinflation. For instance, aluminum is massively cheaper than in 2008, and copper is still quite a bit below the 2011 level. Commodity prices always fluctuate massively.

Corn is much lower than it was 8 years ago, steel is at the same level as it was in 2018/2019, lumber only up 50% from last peak in 2018 (and price fluctuates a lot currently).

This is what is actually so scary. Iirc the petrodollar system has kept American economic hegemony in place for ~50 years but new debt is more likely to be denominated in a mix of Euro, dollar, and RMB. At some point there will be a breaking point in foreign policy (not least of all because the end of American empire has us so focused on domestic fights) and the petrodollar will be over with the signing of a pen. That will trigger a massive reorganizing of the domestic economy and launch China’s primacy.

The trade deficit has also given the US power, and as the petrodollar disappears with fossil fuel no longer being the driver of energy, the US's purchasing power will keep it afloat.

With T-bills trading at negative rates, the US is in a really strong position. People are paying the US for the ability to hold US currency.

This is why I find it so odd that supposedly nationalists in the US rail against the trade deficit and US "debt." Our "debt" is actually just the currency of the world, and as the world grows wealthier and wants to hold our currency, there needs to be more of it out there. This is good for the US and puts other countries at a disadvantage!

It hurts different parts of America to different degrees.

A strong U.S. dollar is generally good for U.S. consumers and bad for people who work in U.S. export industries. The dollar being the global reserve currency is good for the financial industry and bad for everyone else. So basically Wall Street (and workers in industries where America is dominant anyway, like tech, defense, biotech) should favor a strong dollar, while Main Street should favor a weak dollar. This isn't far off from reality: many of the "U.S. nationalists" represent constituents whose jobs have been eviscerated by foreign competition.

In my country young people don't have loans (edit, they may have some nowadays indeed) and we pay for cars out of pocket. Effectively The only loans are mortgages. Young people are not even able to build any debt now because they can't afford a house anymore. So they have a big incentive to see the interest go up again. But I guess this housing crisis is also driven by the insanely low supply, so building a lot more would also help.

What country is this? While I'd like to see consumer debt reigned in a bit, I think not being able to borrow at all for cars is a bit extreme. What happens if you need to buy a car in order to accept a particular job? (If the idea of being a polluting commuter offends you, then consider other job-related items such as office equipment or tools).

I live in the Netherlands, almost every place is accessible by either public transport of bike or (usually) a combination of both, no real need for a car. If you do really need it I'm sure parents are there, a small, ok car can be had for under 1000, right?

If you still live at home you can buy it from your first wage. Otherwise it may take a bit longer. Government advices people to have a buffer of at least 5000 so you can have you washing machine fixed or get a new furnace (the thing that heats your house) and fix other house related issues (or your car). Most people I know try to maintain that buffer.

Maybe a bit, I did indeed have a 6000 eur debt. My knowledge may be a bit outdated. But school (BSc/MSc) will cost a max o 2000/year and the interest is basically zero and you have to pay it back in 20 years if you can't it's forgiven (it was in my time). I paid back the 6000 (parents didn't want to pay for uni) at a rate of 50 euro/month, until I just paid it off in one go.

If you studied for 4 years, that means you only borrowed €125/month. Since you mention your knowledge being outdated, I assume you fell under the old system in which you also received a multiple of that from the government. In today's system that government grant does not exist, except for students with low-income parents.

Student debt isn't quite like other debts though, as you're never required to pay instalments if you don't have the means, and iirc you are also never forced to pay instalments that are more than 10% or so of your income.

Young people have absolutely no power in this society, the fact that the world has come to a halt for a disease with an IFR of 0.25% while entire generations face economic, mental, social crisis should speak volumes.

For me interest rates hovering close to zero since 2008 seemed to be a sign that we had never really recovered from that recession. But I am in no way a financial expert.

An unstated assumption in my post is that productivity growth does not continue apace. When interest rates are low, companies are incentivized to invest in lower marginal productivity investments, because those investments still remain profitable when cost of capital is low. When rates suddenly go up, a number of these investments become unprofitable: the income streams from them don't exceed the new higher interest rates companies would have to pay to roll their bonds. Therefore the central bank is stuck unable to raise rates.

Note that there is another potential ending for this: a deflationary trap like Japan is in, or like the U.S. was in from 2009-2020.

I'm betting on hyperinflation, though. The reason is that nearly all past hyperinflationary events have come from large sector shifts in aggregate demand and aggregate supply, notably when coming down from a war or transitioning from a command economy to a market economy. COVID just provided exactly such a supply/demand shock: large quantities of production were shifted into medical devices and remote work, while demand shifted away from travel, experiences, and gasoline to home improvement & home office supplies. When demand shifts back, those industries will have significantly reduced capacity, and a lot of bargaining power to raise prices. The raised prices cascade through the economy, and that's what triggers inflation.

It's like the economy is your heater, money-printing is turning up the gas because it's not getting hot enough, low productivity is not realizing that your igniter is broken, and COVID is lighting a match. Without COVID you'd just open your windows and air out the gas (although it still wouldn't fix your broken igniter). With it, we go boom.

There is a good article by Lyn Alden on this, but basically, the difference is how the QE is targeted. In 2008, the QE was done in order to get rid of toxic assets and recapitalize the banks - most of that money stayed locked up in the financial system and never made it out (banks had reserve requirements changed and tightened credit, which shrank the money supply - the QE was done to counteract that).

This time around, the banks are well capitalized and the QE is targeted at monetizing the federal deficit (federal government issuing treasuries in order to finance relief packages and the like and FED buying them), so the money is actually going to make it into the broad money supply, which might lead to inflation (though hyper-inflation is probably an overstatement at this point).

Basically Lyn compares what happened in 2008-2009 to 1929 - which was a banking crisis; whereas what happened in 2020 is closer to 1940-1945 / late 1960's in terms of the FED monetizing the debt. We had inflation in the late 1940's and in the 1970s, so it's possible we'll see something similar.

1) 1929 bears no resemblance to 2020. They are completely different economies, and economic factors. It’s a non-starter to compare the two time frames.

2) Inflation != hyperinflation. We can handle inflation just fine, it’s a 5% change, a 10% change, etc. Hyperinflation leads to a collapse (Venezuela, or Zimbabwe or similar). If the United States collapses, you better have stocked up on lots of beans and ammo.

3) We should really only look at historical financial crises as unique events with unique circumstances, not as comparisons. It’s like people looking at home prices now and saying “it’s all going to crash, it’s 2008 all over again!” which is a surface-level analysis that doesn’t take into account how 2007-2008 happened. 1929 - Dust Bowl. 1970s - oil embargo. Etc.

I enjoy reading Lyn’s commentary as well, but the comparisons are non-starters. There isn’t, or so far hasn’t been any predictable events that have taken place. You can’t look at history and say “this thing is the same thing as this other thing”. They just manifest differently.

Because he has no idea what he's talking about. HN people are absolutely clueless on economics but insist on talking out of their ass at every opportunity.

In Zimbabwe the government printed money and handed it out to people. This money directly makes its way into the economy.

In QE the Fed buys assets such as mortgage securities from banks. The banks chose not to lend more aggressively and decided to hold on to the cash. As a result there was no hyper inflation.

So how does QE affect stock / house prices ?

When the FED comes into the market willing to lend to anyone and everyone interest rates fall. As a result returns on bonds and bank deposits also fall. Forcing people into stocks. The effect of QE on asset prices is therefore indirect.

So the QE money itself is hoarded in a deflationary environment while savers get pushed into speculating on assets.

As the economy slowly recovers over 5-10 years the QE money is slowly sucked back out and assets slowly deflate to a fairer value. In theory this can work without too many hiccups.

The problem here lies in the inequality that this generates. Large banks, companies stay afloat thanks to buy backs. Asset owners get richer. Wages stagnate and people lose their jobs albeit less than if QE didn’t exist.

This topic is much more complex than I had initially thought. Nobody should come to conclusions such as “A crash is inevitable” or “Hyperinflation”.

Though I will say, asset prices are not determined directly by central bank actions, there is a third component that pushes both asset prices and central bank policy - the global supply/demand of savings vs investment opportunities. Which is driven mostly by demographics, looking at China in particular. I've commented about this before. There is an interesting hypothesis that the global deflationary and asset price-increasing forces will wane as China's economy becomes more consumer focused and as working age people in China age out of the labor force, thus moving from the net-saving part of the lifecycle to the net-spending part. It's very plausible, unless that population bulge bracket is replaced again by another massive, increasingly-affluent population, say in a fast developing India or Africa.

On the inequality side, it is a bit unfortunate to be in the workforce at this time competing with the massive influx of other savers, bidding up productive assets to save for retirement, enriching the people who were "lucky" enough to be in the generation before that population/affluence boom. But there's not really anything that can be done about it, not without tightening financial conditions enough that it has severe negative effects for the labor market.

Props to you for looking into it! Economics and finance are really complicated. Bank lending decisions are based on risk and profit opportunities, and not at all on reserves availability. QE mostly just substitutes central bank money for the balance sheet "bank money" in M2, increasing reserves and lowering longer term interest rates without flowing immediately into the real economy. Lower interest rates encourage lending and investment, but do not force it. It's a lot more subtle of a tool.

However my worry is that the economy seems to have become permanently dependent on low interest rates. Sure it won’t be zero but something like 1 % looks like a distant dream.

It seems to suggest that we have run out of ways to increase real productivity. A good example is the shale industry which will basically go bust if interest rates are like 3 %.

We seem to be in a new regime of lower economic growth, high asset prices and inequality. The real danger here is the political sustainability of this. Zero interest rates are an indirect pay cut via rents and mortgages. At some point asset owners will have to take a haircut.

It's possible. You are right that productivity growth is the big driver behind everything. There are some people that make the argument that massive growth is behind us, that the internet revolution is not the same kind of game-changer like trains, planes, etc. Not clear how much more "Smithian" growth via trade liberalization is possible, either. If you look at the long histories, there have been plenty of times in the past 2000 years when interest rates and economic growth were very low for an extended period of time. Inequality tends to grow to it's maximum sustainable level in between catastrophes, though that level is likely lower now, because there is a certain amount of disperse affluence necessary to sustain the modern knowledge economy that creates that wealth in the first place.

But at this point, we're talking technology and society instead of economics. Will innovation continue, and are those innovations a big enough deal that they will continue to make our world more productive, wealthier, more successful? I lean towards yes, but it is not at all obvious. It is certainly possible that productivity growth stagnates, most countries catch up to a generally-developed level of output, and asset prices stagnate as temporary demographic bumps are smoothed out.

My personal belief and this is where a lot of people might disagree with me is that we will not see the kind of growth we saw again.

Growth is fundamentally tied to the availability of cheap energy. If you look at oil prices in gold you’ll see how it’s almost twice as expensive today.

We are also facing constraints on energy extraction due to climate change.

Every time oil prices spike shale oil comes online but the economy chokes on the price oil crashes and the shale producers go further into debt.

This may also be why a lot of growth is in the digital sphere which is far less energy constrained. Maybe future growth will be Virtual reality GDP :P

The only way I can be wrong is if someone invents a cheap fusion reactor or a cheap magical battery that stores endless amounts of solar energy. This is highly unlikely to happen.

Disclaimer: Very speculative thesis but I believe in it.

I don't necessarily agree, but doesn't the parent comment clearly say:

>I'm betting on hyperinflation, though. The reason is that nearly all past hyperinflationary events have come from large sector shifts in aggregate demand and aggregate supply

The user is arguing that large scale shifts in aggregate demand and supply are what is different this time.

When demand shifts back, those industries will have significantly reduced capacity, and a lot of bargaining power to raise prices. The raised prices cascade through the economy, and that's what triggers inflation.

Not sure I buy that. Yes, there will be temporary upwards pressure on prices in some segments of the economy but also, following your argument, temporary downwards pressure on prices in other segments. So a) it's going to balance out and b) it'll be temporary. Not enough to trigger sustained inflation, not nearly enough to trigger hyperinflation.

Are we going to see higher inflation in this decade vs. the last? Absolutely. But hyperinflation is a different beast altogether and I'm quite skeptical we have the environment for it to come alive.

I don’t know about your reduced capacity argument. The reason Buffett sold his airline shares so low is he foresees supply outstripping demand for quite some time in the industry. Presumably that would apply to other travel/experience stuff as well. And for gasoline I think the Saudis et al can ramp up preeetttyyy quickly.

I think the airline industry is sort of uniquely vulnerable vs other travel/experience related industries: in the short term, supply may outstrip demand for some time against a relatively fixed cost base; and in the medium term, there may be limited ability to scale back up rapidly if airlines are unable to re-recruit pilots and crews they had to let go to deal with the short term.

> If everybody has an incentive for rates to stay low, they will stay low

Your list of stakeholders who like low rates is the same today as it was in the 2010s, the 2000s, the 1990s, the 1980s and the 1970s when rates were much higher.

If stakeholders who like low rates had the power to set the rates, the rates would have been lower then, too.

> This ends in hyperinflation

Counterpoint: low rates are a consequence of a sluggish economy, not Soviet-style central planning. If the economy comes roaring back with double-digit GDP growth eight quarters in a row, and central banks continue printing tens of trillions of new money in the face of an overheated economy, then we'll see a wage-price spiral. But if the economy remains sickly, or central banks ease off the stimulus, then it's hard to see hyperinflation on the horizon.

I generally agree with your comment. However, retirees should want rates to rise. As you age, you want less of your money in more risky assets like the stock market. You want your money in CDs, money market accounts, and bonds. You want these safer instruments to pay a decent interest rate (say 5%) and not 1%.

However, as you point out, rates have been low for a long time. This has caused retirees and people approaching retirement to invest in riskier assets. They have been forced into a loser’s game. That’s going to cause a lot of pain if we get a massive correction.

Those of us who have time to recover from a correction will be OK. Those who lose 50% of their assets in a correction, and don’t have the time to make that up, are going to have their lives turned upside down.

If you already hold fixed income assets, you do not want rates to rise, because when rates rise, the price of your holdings will fall. When rates fall, those interest bearing assets look better in comparison to the new bonds (e.g.) that are being issued, so their price rises.

That is correct, if you are currently holding with the idea of selling before maturity. However, if you are holding to maturity or investing in money markets or CDs (that are short-term), you do want high interest rates.

Imagine yourself in 1981 and could have locked up a 30 year U.S. treasury at 14.5%. Sure, there are riskier investments that may have beat that. However, if you are a retiree, that type of consistent, non-risky return is what you would want.

When you sell doesn't really matter. The current value of your bonds (e.g.) will still drop if interest rates go up.

If you bought that 30 year at 14.5% and we had hyperinflation then you wouldn't be so happy. There was a reason why those rates were at that point, inflation was >10%.

Conversely you could try to short bonds now but if rates stay at zero for the next few decades or go negatively that's not gonna be so great. In the rear-view mirror someone will say how we were stupid(?) for not shorting bonds when the rates shoot up to >10% again, or they don't. It's hard to win this game.

What is true is that retirees might have a shorter horizon (though people keep living for longer and longer) and so they may be forced into safer/shorter duration investments and possibly into smaller returns.

While this is true for an individual investor, a large part of the market for fixed income investments is large investors who are liability matching in one way or another: either against a portfolio of life insurance policies or against defined benefit pensions. They genuinely don't mind if the value of their bonds falls due to rates movements because (if they have done their jobs right) the value of their liability stream will also fall by a corresponding amount.

Of course, you can then apply your argument to people who have pensions or life policies I suppose but those aren't things people often "sell".

The system is structured to prevent even the slightest bit of inflation by raising rates. The Fed has not forgotten that, and the politics of mass unemployment are readily manageable. Years of conservativism has seen to that. Call me back when inflation exceeds 4%. It's currently below the 2% target.

Look, interest rates are the market price of money. Money - investment - is not scarce. That's where the asset bubbles are coming from, after all. And it's not just a question of money creation, it's wealth creation and concentration that's driven this. Everything from Apple's cash pile to the unaccountable wealth of Saudi and Russian fossil fuel extractors to all the capital flight from China that's been bloating Western real estate markets.

The world is awash with money looking for a return which it simply can't find any more. Maybe my most controversial opinion is that if we don't get wealth taxes we'll end up having to have negative interest rates anyway. Something has to pay for the preservation of society around the pile of wealth. Switzerland has been doing good business charging people for stability with negative rates: https://edition.cnn.com/2020/01/23/investing/switzerland-cas...

Let's not forget the pension funds. Something like a third of a Western society is basically forced to be bond investors - they need low-volatility investments and annuities.

> Retirees have an incentive to keep them low, feeding 401K bubbles that they need to live on.

... they tend to be the main complainers about low rates since they live more off interest rates than asset prices and don't have mortgages.

Don’t forget that municipalities are counting on interest rates staying low so that assessed values of homes can stay high and property taxes remain high. If interest rates were to cut home values in half then numerous municipalities would face extremely hard decisions or even bankruptcy.

Interest rates have declined for 40 years. There is no reason to believe they will trend up long term. I don’t know if it ends in hyperinflation though as the number of people that can access the cheap money is limited.

Federal Reserve act of 1977. Dual mandate: price stability and maximum sustainable employment. Inflation around 2% and unemployment under 4% pre-COVID doesn't smell like failure to me, but that's up to you. Especially if you compare to other developed economies with even more sluggish inflation and insane unemployment rates since 2008.

That's not how employment works. There is a certain amount of natural unemployment even in a full employment economy: this is called "frictional unemployment." Like, you just moved or quit your job or got laid off and are looking for a new one. You are unemployed for a couple weeks or months, or longer if you're retraining. There's also structural unemployment, people who are unemployed (or underemployed) because their skills are not suited to the current environment. Central banks can't do anything about that with interest rates. There will always be some people unemployed.

Full employment is defined by the concept of the NAIRU, the non-accelerating inflation rate of unemployment. The lowest sustainable unemployment before inflation begins to take off in a feedback loop (as higher inflation pushes expectations of future inflation up, resulting in a spiral).

Yeah, there's a big fight about this - AngrySkillz is entirely correct about "NAIRU", but it's one of those parameters that's difficult to measure because you can only find out when it's "too late".

Heck, even the "4%" is a percentage of people "looking for work", which is obviously a quantity that can vary depending on how good or bad the outlook is.

>> There were no interest rate hikes between 2006 and 2015, and interest rates have been at zero for 8 out of the last 13 years.

Right. The increase in 2005-6 was what set off the 7'8 financial crisis. I never understood that one. The previous cuts seemed like an over reaction to the tech bubble popping, but the rapid rise was even worse.

I thought they were very slowly raising rates prior to Covid, but using housing market to judge how slow to raise them.

The Fed can only directly set the Federal Funds rate, which effectively allows them to set a floor on short-term interest rates. Short term rates influence longer-term rates, but the longer you go out on the yield curve the weaker the effect. So, yes, while the Fed wants lower interest rates generally because lower cost of capital is good for growth, the Fed cannot artificially will long-term interest rates to be at a certain level.

Eventually, the yield curve will start to look somewhat normal again, and we'll start to have a yield curve that rewards longer-term fixed income investors. Longer-term interest rates reflect market forces, and eventually investors will demand higher yields for longer-dated US government and corporate debt.

Finally, though I increasingly see the term "hyperinflation" thrown around in conversation, hyperinflation in the US is just not even a remote possibility. The last time an actual hyperinflation occurred in a major economy was Germany after WW1. The differences between then and now are too many to mention, but here are a few: fiat current vs gold standard, reserve currency status (the US today), massive debt burden denominated in a foreign currency (Germany then), immature and non-independent central banking (Germany then). A Weimar Republic style hyperinflation is just off the table; so let's stop throwing the term around.

Maybe you're referring to something akin to the US 1970s era "very high but not event close to hyper-" inflation, e.g. 5-20+% per year. While possible, it's highly unlikely. Maybe we get to something like 5% annualized inflation for a year or so, but I wouldn't bet on much more than that.

The inflation period in the 70s (stagflation) perplexed monetary policy-makers at the time, who weren't used to seeing high inflation coupled with stagnant or negative growth. This period of inflation was caused largely by market characteristics that simply don't exist today: energy price shocks that caused raw materials supply constraints throughout the economy. The US was a much more concentrated economy in the 70s, with a relatively large portion of GDP tied to raw materials and thus imported oil. Today the US is largely energy independent and does not have such a narrow concentration of supply dependencies in the economy. The US has evolved into a much more diversified and service-based economy, as opposed to the manufacturing-focused economy of the post-war period. There is no one commodity that we rely heavily on that, if unable to access would effectively stagnate economic growth. In the 1970s, OPEC basically said, "hey, no more oil!", and we were like "yea but we need it for pretty much everything and if we can't have it we're fucked" and OPEC basically said "yea well tough shit".

There is not a modern equivalent of imported oil that is the lifeblood of the economy controlled by a cartel that when supply is artificially constrained we would be completely fucked. Even something like semi-conductors while worrisome, is fundamentally different than a commodity like oil. We can decide to produce semi-conductors if it's in our economic interest, but we can't just decide to have more oil.

Finally, central bankers are not stupid. They're very aware of inflation risks. And while they are committed to keeping short-term interest rates low for an unusually long period of time, long-term interest rates do and will reflect market conditions.

This does not end in hyperinflation; it ends with moderately elevated inflation and that outcome is undeniably better than a deflationary outcome.

All this is because money lending is a business. We've known for literally thousands of years (Islam, Judaism, Christianity at least) that lending money with interest is predatory, harmful, and destructive. Couple that with the government being able to print money at will to cover its ever increasing debts (again, due to interest), and we see how the hole keeps getting deeper.

It saddens me that we don't learn from past wisdom, and that greed drives the world. We see people vouch for clean energy, what we also need is clean finance and economics.

Lending money at predatory interest rates is predatory. Lending money at interest, full-stop, is not predatory. Just because an activity was widely condemned by ancient religions does not make it evil in fact; see homosexuality.

Further, these prohibitions originated in a different era, an era centuries before the existence of anything approaching modern finance. For instance, in the Roman era, loans were a purely private thing, and from what I could find, the rich elites who would loan out money would do so at rates potentially approaching 48% per year. It's fairly easy to see how a mostly poor, mostly minority religion during the time of the Romans would consider this practice sinful, considering it was likely a common tool used against their communities. As more modern commercial practices began to slowly form in the 1600s or so, average interest rates began to drop, and with it went much of the prior vehemence against usury.

Interest is what encourages a bank to lend me money now so that I can afford to build a house. The total value of the house is $200,000. I am willing to make a bet that over 30 years, I will earn enough that I can afford the purchase price of this house in present value dollars. However, the people building my house need to be paid now; materials need to be purchased now; and so on. Not in 30 years, but now. Who in their right mind is going to give me $200,000 to use now with no promise of recompense? At the very least we need interest to cover risk.

People no longer live in houses that they can build themselves with a modicum of diligence and work. (I am using houses here as just one example, but you get my point.) We have an unimaginably better standard of living than we did 2000 years ago. A large part of how we pay for that is interest. I'm just not clear how we could keep living in anything approaching an approximation of our current world without the existence of interest. Having idealistic visions of constant charity is not workable.

This is literally a logical fallacy. We see the evils of interest every time the topics of wage gaps, national debt, and so many others come up. Yet, it seems most people are blind to it, and try to patch the system, not realizing one of the core contributors to the problem.

This is a very interesting point, and everybody should look at this! But I would also counter that everybody should read David Graeber's book "Debt: The First 5000 Years" as it covers this and much much much more. Probably one of the most interesting books on the concept of money and lending and how human societies have organized around it.

Please note that not all "Sharia-compliant" financing models are in fact, Sharia compliant. As a matter of fact, many of them aren't (unfortunately). What ended up happening is that many so called "Sharia compliant" solutions are simply changing the names (and some minor mechanisms) of modern day usurious offerings (e.g. bonds, mortgages), and then slapped the "Sharia" label on them. However, talk to proper scholars and they will tell you that they're nothing but usury in disguise.

That being said, I've seen some good attempts at producing proper Sharia compliant offerings. But most people will not want them, because they have true risk sharing, unlike the modern financial system which feeds off the poor and widens the gap.

They absolutely are "usury" in disguise because usury is defined as lending for profit and forbidden and the governments of these countries have acknowledged that they cannot run a modern economy and develop a modern society without allowing for lending for profit, but they cannot admit this because there are serious consequences for admitting that the book is wrong on this topic.

Define "true risk sharing", if you mean what I think you mean, the opportunity for a borrower to file bankruptcy is true risk sharing.

Many of the governments you're referring to have been installed by the West. They're either too lazy, or more likely, forced by the West not to implement a proper Islamic financial model. The ones that haven't been installed by the West are constantly fought to prevent them from prospering.

Running an economy without lending for profit has already been proven to work, so the Book (Quran) most certainly isn't wrong about the evil of interest. Just look at Islamic history until post WWII and the fall of the Ottoman Empire, where colonialism followed and the occupiers brought with them and force installed their usurious financial systems. Even if you look at non-Islamic experiences: https://www.youtube.com/watch?v=Io2a4SOX22Y

True risk sharing is where there is no contractual obligation for the lender (or "investor") to profit. Islam declares that any loan that produces any sort of benefit to the lender (tangible or intangible) as Riba - a term used to encompass a class of impermissible financial transactions which includes, but not exclusive to, usury and interest.

You can't really discuss usury in a modern context without taking into account, the entirely modern notion of what money is. I.e. the instrument of today's national currencies are entirely detached from what used to be considered money, which was what the concept of usury applied to.

More specifically, when the government openly inflates the money supply by a certain percentage every year, then investing your cash into T-bills could suddenly be seen as merely a defensive move, to protect your holdings, rather than a usurious transaction with you as the benefactor.

I am not arguing that point or another, but this is just one example out of many where the issue gets confused by the complications of the modern financial system. It could well be argued (and many do) that large swathes of the financial system is incompatible with Islamic principles, and that the only acceptable option is a radical reimagining of these structures. In that, they would agree with a growing secular movement who are increasingly discovering that the monetary and financial system is stacked against them, and enriches the few at the expense of the many.

I guess what I'm saying is that it makes little sense to rail against 'usury' while ignoring the realities of the 'modern' nature of money.

> I.e. the instrument of today's national currencies are entirely detached from what used to be considered money, which was what the concept of usury applied to.

True. Which is another core problem. We should go back to proper money, not what we have today.

Let's take a step back. Why did the governments decide to detach money from gold and other metals? It's because they want to be able to print money at will to cover their ever increasing debts, due to interest. What effect does this have on the average person? They work hard to save money, only to have their savings devalued because of someone else's greed and incompetence. This is not sustainable.

That sounds like the "not real communism" argument. "Not real sharia". I would argue that SA is absolutely real sharia, and they have schemes to allow mortgages that function basically like lending but avoid mechanisms that would look like lending for profit by the letter.

The problem with rules against lending for profit is that you have no incentive to let anyone use what you have for their own benefit. If someone comes to me with an awesome business plan and wants some money, if I want to help them I am going to expect them to take the risk on their business plan rather than subject me to it.

What's SA? Saudi Arabia I presume? Are you a scholar to argue what is and isn't compatible with Islamic laws? We go back to our texts (Quran, Hadith) to determine whether something is or isn't compatible with Shariah. There are explicit texts that prohibit increasing the price of an item in exchange for a delay in payment.

> you have no incentive to let anyone use what you have for their own benefit.

Renting is a trivial counter-example.

> if I want to help them I am going to expect them to take the risk on their business plan rather than subject me to it.

Which is specifically one reason why lending with interest is prohibited. You don't get to profit off of the need or misery of others. There's a power dynamic difference that Islam aims to make more even. We've already seen countless times how this ended up throughout history. And we're living it today.

I'm not a scholar, but I'd guess that the Saudi government consult scholars and their government is probably more knowledgeable than either of us on this topic. You discredit their rules by claiming that they were installed by the west (which does not matter, either they follow sharia or they don't) and then appeal to scholars. Sounds to me like you want your idea of sharia and anyone who disagrees "needs to consult a scholar".

I've always disliked this appeal to scholars in Islam because Islam likes to set itself apart claiming there is no pope or interpretive authority on the law of God and then any time a person has a disagreement they appeal to an authoritative priesthood class to stifle discussion on issues that matter. For a religion that bills itself as easy to understand by the common follower of the religion, deference to human beings as authorities are quite common.

Any lending for profit is dangerous and predatory. You mock religions, but fail to defend your point. We're literally living the destruction and huge gaps and wage issues caused by interest, yet no one is batting an eye. I feel sorry for humanity at times.

You're arguing against a strawman. I never said that people will be forced to lend money without compensation. With 0% interest rates, any lending will be purely out of charity. If people want to make money, they will invest it, as we've been doing for millenia. Invested in moral ways.

There exist today developers who will sell property in installments, without upping the price. I've seen this in at least one West Asian country, and I wouldn't be surprised if it were more commonplace.

I'm not who you're responding to, but you've yet to defend your assertion, that lending for profit is always predatory, and your assertion that "we have known for centuries" by way of bronze age cults (in my opinion) that this is indisputable fact. It isn't indisputable, defend your point.

I'm not calling you stupid or anything like that, but you're showing that you do not quite understand how lending and markets and even investing works. You're ignorant on this topic and I strongly advise you to do a lot of reading on it.

I'm aware of how things work. The fact of the matter is that even if we go back not long ago to pre-WWII, we see a certain individual produce a huge economic recovery by banning interest, among other things: https://www.youtube.com/watch?v=Io2a4SOX22Y

Lending money is absolutely essential to the development of any society. Lending is not predatory by it's nature, or harmful, or destructive. The US for example would not have coast to coast and border to border high quality road and other transportation infrastructure if not for lending. This infrastructure increase the productivity of the nation, allowing that debt to be paid back, decreased the cost of transportation for everyone and increased the standard of living for everyone in the US.

Think of it like this: if you are borrowing money for anything that does not increase your productivity, you're making a mistake. If you're lending money to someone for something that does not increase their productivity, you're increasing your risk of default substantially.

It isn't about greed, fact is, sometimes people need money they don't have, and sometimes people have money they don't need at this very moment, and if both parties make a good, sound judgment, both can benefit from this scenario. Every day people make their lives better by borrowing money. The view that lending and borrowing are innately bad is a very narrow minded view, one based on ignorance of the facts of how lending works.

Depends on the size of the society. If you think about it from scratch, you only need lending once society grows to about a certain threshold where you're essentially dealing with unknown people. Interest is a compensation for the risk you take, combined with the loss of investable capital during the loan period. It's quite different from helping your friend or relative build a house, along with a dozen other members of your society, with the social agreement that that friend will help you out when you are in need. Most of our societal issues I think stem from stepping above the size of our social circles.

It's not ignorant, otherwise it would have been prohibited by Islam, Christianity, and Judaism, among others probably. This video is telling: https://www.youtube.com/watch?v=Io2a4SOX22Y

If you want to build and prosper, you can find investors willing to put money into your project or business. Lending money is not the only way to prosperity, as evident by how we had an entire empire (the Islamic Empire) that prospered and was at the forefront of many fields, yet did not deal with interest.

People simply want the easy way out, and lending with interest is the easy way out in this case. It's intellectually lazy, and has caused destruction time and time again throughout history. But people turn a blind eye because of the relative few who stand to benefit greatly from interest, at the expense of everyone else.

How do you feel about the government being able to print money at will and devalue the dollars or euros you worked hard for? You can thank interest for that.

I know YC purchases equity rather than debt with its investments (and that equity stakes are rarely considered "usury" and not always considered "lending"), but it's a little odd to see this comment on a forum hosted by a venture capital firm, whose whole business is about letting people have some money in the hope of profiting from it later on.

Purchasing equity is the moral approach. This means that the investor also bears the risk. If the company succeeds, the investor makes money, if it doesn't, then he lost money.

> but it's a little odd to see this comment on a forum hosted...

Why? They're not lending money, they're investing, two very different things.

Not entirely. VC exists for things where debt doesn't work. You can use debt to fund some things, eg. real estate, because a failed business still has a valuable asset to sell.

If a vc funded tech company goes under, the only thing to sell is source code, which is not nearly as fungible.

I'd argue that's a consequence of creditors bearing the risk of default. The risk is high both because the business may go under, and because the business has few assets that can be liquidated.

Yes exactly, its exactly the reasons you said, high risk and few assets.

> creditors bearing the risk of default.

The person giving away the money is always bearing the risk, that doesn't go away. VC will bear the risk still.

With an interest bearing loan, the bank will come after the borrower's assets, seeking not just the principal, but the interest on top, until they milk them dry.

This is just one reason why lending money with interest is immoral. Read up about Islam's position on this issue if you want to learn more. It's quite eye opening, and sad that we have to live in a world that is based on fundamentally evil and corrupt financial practices.

Haven't western countries typically addressed the issue of protecting borrowers through corporate entities and bankruptcy protections?

If my company borrows money, then goes bankrupt, the lenders cannot come after my personal assets unless I've personally guaranteed the loan, or broken certain rules about mixing personal and business accounts (allowing the creditors to "pierce the corporate veil"). In personal bankruptcy, my primary residence and vehicle are protected up to a certain value, along with retirement accounts.

It certainly doesn't seem like a pleasant process, but at a theoretical level the rules generally seem fair to me. One huge problem is that people don't know the rules, a situation which I suspect lenders and debt collectors are happy to encourage. There certainly are a lot of corrupt financial practices, but I think lending money can be done fairly (at least in theory). I find other perspectives on the matter very interesting. I'll be sure to read some more about Islamic finance!

> I'll be sure to read some more about Islamic finance!

Be careful about what you read. As I mentioned in several comments here, most so called present day "Islamic finance" isn't actually Islamic. Don't let labels trick you.

Are they condemning sukuk? I thought sukuk was an attempt to reconcile the desirable qualities of a loan with Islamic jurisprudence surrounding finance?

So unless the commenter thought sukuk was illegitimate (I haven't seen them state this, maybe they have), wouldn't it be reasonable assume they consider sukuk acceptable?

Perhaps obviously, I'm only vaguely aware of Islamic finance, so I may be missing something basic.

*EDIT*:

I've just seen the comments where they appear to be condemning sukuk, or at least common implementations.

But it seems like their point is that they think it's simply slapping a different label on lending, which I'm inclined to agree with (especially if there are repurchase agreements and guaranteed returns).

A lot, if not most, of present day "Islamic finance" isn't compatible with Islam. They're simple relabeling of Western practices with Arabic terms, but underneath they're more or less the same. There are many Hadiths and narrations prohibiting and condemning these actions.

So ghazwa is a preferable alternative for economic growth. Gotcha. Let me know how taking potshots at NATO in Syria goes. How are you any better than Western colonialists then?

It's well known that many Arab governments today have been installed by the Western colonialists. It's established history. We're still living the effects of post WWII colonization and Sykes-Picot. Of course, there is blame on us too, but to deny external influence is also ignorant.

This position is unpopular (referencing religion on HackerNews, oof move), but I think there's more wisdom in it than those who dismiss it immediately by referencing religions stance on homosexuality are seeing.

Lending is absolutely critical to our economy. But that's not what we're talking about; what we're talking about is lending with interest. And right now, we're in a discussion here about the Fed hitting 0% or near-0% interest rates. Its absolutely a valid train of thought to consider.

I don't have the knowledge or skills to comment on why it may be invalid or valid, but I do believe that its a worthy point of discussion.