"It turns out to be really good for a company to have a board -- it focuses the company if everyone knows they have to present the key metrics to outsiders once a month. ... If I could ask VCs for only one thing in this new world, it’d be to keep showing up for board meetings."

This is very interesting. If ownership percentages at Series A are trending down, and investor time & emotional investment per company is trending down as a result, but having outside accountability predicts success, then I wonder how the best companies will replicate outside accountability.

Put another way: How could you hack a replacement for a board meeting?

I'm a funded entrepreneur without a board. I've tried nominating advisors and/or very-helpful angels as our "pseudo-board" and meeting monthly. This didn't help very much: There's something about having a lot of skin in the game that makes board members really prepare, take it seriously, and summon courage to have hard conversations with CEOs when things aren't working.

The one thing that worked pretty well was bolting a whiteboard over the desk area with this month's single goal (a revenue number, natch) and value so far. I don't have any board experience to compare it to, but it certainly keeps us focused.

Anyone else have ideas that have worked, or might work?

Your board (and VCs by extension) are not the only accountable 3rd-parties... I'd argue that they're not even the best accountable 3rd-parties because they're interests are not necessarily aligned with yours - VCs have limited partners to worry about.

Look no further than your customers for great 3rd-party accountability. If they love and use your product, they will pay you more money and recommend you to others. They should be the only thing that matters. In fact, by not having a board you have the luxury of only being accountable to them.

We just did a late-seed round from a VC firm and didn't set up a board.

Something that has worked for us is doing a bi-weekly Google Hangout that has no agenda. The rule is no one prepares for it, but we just talk about stuff at a high level. So far it's been really helpful. We don't feel unnecessary pressure to prepare decks with stats and metrics on things that aren't important or will be changing quickly (plus I have the key ones memorized anyways), yet we communicate frequently enough that issues can be tracked closely and fixed.

It also works that we had only one firm in the round so coordinating it is easy. Might not work if you have lots of angels or other investors.

Of course we talk metrics, we just don't prepare them formally. And we don't have to because our dashboards are pretty much real time anyways (which we sometimes jump into through screen share).

My guess is that the knowledge that you will get feedback is significant, because the worry about what the feedback will be like forces you to focus better. That said, public transparency probably has the same effect.

The fundamental questions seems to be (1)"what is the purpose of a BOD"; and (2) are the "good things" the primary purpose of the BOD or the emergent phenomena that happen as a result of (#1). In other words, will (#2) type events happen outside the context of (#1). And this includes changing (#2) type things to be (#1) at a formal level.

The valuation bubble will eventually burst -- the question is when?

The gross over-valuations occuring today are not sustainable -- the companies that are being purchased for billions USD are not actually worth that much. $16 Billion for an instant messaging company, $2 Billion for a research company with no product. Now everyone feels they are worth Billions when in fact, not only 3 years ago these companies would have sold for maybe a few hundred million USD at best.

I see them as merely a correlation of the overvaluation of tech companies, not a continuation of the bubble cycle. Most of those huge acquisitions are done with stock, and if that stock is overvalued, so is the purchase price, even if the purchase price was correctly valued once you control for the price of the stock.

Take WhatsApp's acquisition which is the holy grail of overvaluation. If you think Facebook's stock is way overvalued, then Facebook may have correctly valued WhatsApp's price. If you remember it was initially announced as 19b before Facebook's stock devalued it to 16b in the face of the seemingly hilarious overpay.

A lot of the "real money" startups generate is from selling services to other startups and tech companies - particularly in the YC ecosystem. It's possible that revenue will slow in a crash and start a nasty cycle.

That's exactly what happened during the 2000 crash -- much of the "revenue" being booked by internet companies was imaginary (in the form of contract swaps), and much of that was driven by intra-industry advertising. Everyone was paying everyone else to advertise, and it all fell apart more quickly than you'd expect given top-line revenue numbers.

I suspect something similar will happen this time around -- there will be a slowdown in the real economy for some unpredictable reason, and the imaginary, startup-servicing-startups economy will implode.

This is an important observation. There are absolutely angel and venture-backed startups with "real" revenue (fewer with actual earnings), but if you look closely, it appears that a non-negligible percentage of them derive a not insignificant portion of their revenues from sales to other angel and venture-backed startups.

More broadly, an even larger number of startups are also indirectly dependent on the current landscape, as they operate in regional markets where consumption is being driven in large part by the influx of capital into tech.

There's nothing wrong with building a business that takes advantage of these types of situations, but my sense is that a lot of the entrepreneurs running these types of companies aren't consciously aware that they're the beneficiaries of an environment that will eventually change. As such, they're not at all focused on trying to diversify their revenue base and to be frank, it many cases there really isn't an opportunity for them to do so anyway.

To YC's credit, it's incredibly hard to sell anything to the YC ecosystem from outside of it, because they already have chosen options from inside of it. Yet another reason to give radical differentiation a shot if you can stomach it.

It's interesting to see a post discussing how free VCs are in their investments as I'm sending out job applications because we couldn't make it past the Series A crunch despite big-name customers and ex-FB/Googlers on the founding team.

Make no mistake, VC firms may be increasing the capital they're investing in the markets but by no means does that translate into "everyone gets a free ride".

Is there a decent way to calculate valuation? We're starting to be approached with merger/acquisition talk and we're unsure on how to best determine our value in that scenario.

We're a 2.5 yr old company, annual revenue for this year forecasting to $1.1M. (2013 was $360k, 2012 was $60k). We're a team of 5 salaried employees (founders included), bootstrapped, fully employee-owned and steady revenue growth with very low operational costs.

Meritt,

ignore DCF's - they are utterly useless in the tech / venture world, especially at the stage you're at. Look at it more as "what value are you providing to the firm" - everyone and their grandmother will claim that its strategic (ergo, justifying high valuations with non basis in financial reality), but very few can pull that off. Failing that is if you can show how valuable you can be to that firm - ie, to use a simple example, if using your approach can provide them with a 5% uplift on their typical sale). Otherwise, its an opportunity cost thing for you - what is your logical upside at a more mature stage, and what is your self-perceived probability of getting there? You don't have to sell, which makes it very powerful.

"Meritt, ignore DCF's - they are utterly useless in the tech / venture world, especially at the stage you're at."

I wouldn't say they're utterly useless. The thing is, they're starting points. DCF isn't the beginning and end of a valuation process; it's a guessy data point. But it's more educated than a lot of other guessy methods. At the very least, it serves to ground the acquiring company's expectations.

I wouldn't rely on a single, straight-line DCF for a startup. Ever. But model out a few scenarios, and play around with a few factors, and you arrive at a sort of distribution of outcomes. That distribution requires an an asterisk, but it isn't useless.

Also, in the event you're being bought by a publicly traded company, somebody there needs to present some sort of NPV-based analysis to someone. If you're a small acquisition, that may be a mid-level manager to the VP level. If you're a big acquisition, that'll be the C-level to the Board (and indirectly, to Wall Street).

Here's one way to figure out the valuation of your bootstrapped company.

If you continue running the business and pursue your current operating plan, how much cash will you have in the bank in year 5 and year 10? (Broad estimates are fine)

Generally speaking, your year 5 and year 10 estimate is going to represent a reasonable approximation of your company's valuation range.

For example, let's say you believe you will have $5.5m in the bank in year 5 and $12m in the bank in year 10. Your valuation will approximately be $5.5m to $12m.

Financial buyers will generally offer $5.5m. Strategic buyers will generally be willing to pay $12m or more depending on the prospective synergies/option value of the assets.

That said, you'll need to ask yourself how much money are you willing to accept today to walk away from $12m over 10 years. Are you willing to accept $5.5m in exchange for more freedom/time to devote to other things that may add more personal/financial value over those 10 years.

(Many startups are optimizing for high option value and this approach might not be appropriate for those companies)

Comparables are good, but you may also want to check out Aswath Damodaran's work. The simplistic version is to do a discounted cash flow analysis and use comparables to get an idea on the discount and other variables.

What have comparable businesses raised capital at? Think about it as a calculation like V = P x M (Valuation = Profit x Multiple; sometimes you'll use Revenue instead of Profit). The Multiple is the magic number.

I'm helping a seed round at present, and we managed to find several 'competitors' who raised several rounds each at a fairly consistent Multiple. We have subsequently used that to explain the discount valuation we're using.

Crunchbase is a good place to start, and in a big enough market with good google-fu you'll be able to gather the data to support a Valuation.

Generally speaking valuation is speculative. Think of it this way - a gallon of milk is priced at $3 because that's the price people are willing to pay for it. If it was $10, no one would buy it and if it was $0.01, they'd run out of supply. Same thing goes for business. The valuation is whatever people are willing to pay for it. If I buy milk for $3 it's because I know if I consume foods right now it will give me energy so I can do more things later in the day. Some people create a story speculating that a particular gallon of milk has the ability to give you twice the energy, so they'd price it at $6. These stories turn out to be true sometimes and sometimes not. Hence, why today valuations are considered crazy because everyone is painting a unicorn story.

A few factors go into valuing a company, which potentially aid the craze:

1. There is extremely low liquidity in non-public markets for investing. In other words, you don't have a millions of people in the US investing in startups every day. In a perfectly elastic market, valuations are 100% correct. Due to the high liquidity and number of actors, public markets are much better at reaching perfect elasticity whereas private markets are not. In other words, less actors dictating how much they are willing to pay for something means higher deviations from the true price.

2. Many tech companies are irregularly (irregular in relation to existing companies) evaluated today because they do not follow traditional investment metrics. This is largely set by precedence. When Facebook and Google IPO'd, the investing community was fairly clueless as to how to evaluate these companies. The metric they've chose is DAU/MAU because it translates into how much attention "land" they can acquire to resell to advertisers and hence increase revenues and profits. Now that these are "the metrics" it means every other "tech startup" is in a land grab to attain those numbers quicker anf faster than before. This is why Instagram and WhatsApp had such high valuations...their DAU/MAU's were crazy high and growing at faster rates than Facebook itself.

Generally, the larger investing community values companies based on earnings. EBITDA is usually a popular metric to do this, but one metric can't dictate everything about the valuation. Valuations are based on a series of metrics, a multiplier, all based on the speculative return of buying the business. So for example, a company a one-year $1.1m budgeted forecast might be speculate to be worth $5mil simply because the revenue growth trajectory means they can return. Now add in a multiplier of 2.2x because your team is a group of badasses and your contracts last 3 years, and bam your company is worth $11mil.

Because tech markets have high growth potential (Uber is quoting to having had doubled their growth every 6 months) it means the valuations are abnormally higher than many other businesses. How many hair salons do you know that are doubling revenue every 6 months and have relative businesses who have shown similarly consistent growth in that market?

All things being equal, the question ultimately becomes "what part of the hockey stick am I on?".

>If it was $10, no one would buy it and if it was $0.01, they'd run out of supply. //

Do you think? Milk is a pretty much fixed use rate for homes I feel - low cost milk is probably more a loss-leader than anything else. If there's a crisis in the dairy industry those who can afford to pay $10 probably will for quite a time. The reason my supermarket doesn't charge more is competition. Milk is fungible, largely, hence competition plays a more important role [we buy Organic milk wherever possible however]. Most tech isn't so fungible.

I guess how that feeds in to your valuation analysis is that USP is important? Even if your business amounts to just another messaging app, or another photo app, you can have a USP - like Whatsapp's user base?

... if milk were 1¢ I'd take up cheese making; cheese is so expensive.

compare your revenue growth rates, earnings growth rates, gross margin and other metrics to similar public companies. Then looks for a price/sales figure (or forward price/sales figure). Based on the info you've given, your company is probably worth around $20 million at the moment.

"Resist the urge to raise and spend too much money. The track record of companies that raise $30MM or more in their first round is bad."

Q: Is the track record bad, or do they just fail louder than the ocean of companies that raise small amounts of $ and then quietly die? It'd be interesting if someone could prove that a large raise actually hurts your chances, but for a disciplined/veteran founder (who would raise a lot but spend it thoughtfully rather than recklessly), it seems like it shouldn't.

It may also be related to the fact that the get-big-quick scheme is inherently risky in order to return the necessary rewards. If you're raising a ton of money you have to be a home run, and that means you may pass on moderately profitable opportunities in order to keep looking for insanely profitable ones.

sure, but if you haven't taken a ton of money, you have the opportunity at some point to take a strategy that turns a small, steady profit now instead of being continually forced to doubling down on being the Next Big Thing

Good luck aligning those goals with investors'. Most of them signed up for the Next Big Thing, if they wanted a small steady profit, they would've bought a condo and rented it out.

Your point about fail louder is probably right. We dug into data after Sam made this statement and the data suggests there is not much of a relationship b/w initial funding and successful outcomes.

* Interest rates are kept low primarily because of the unemployment crisis. (Right?)

* But then that encourages capital-holders to invest in, among other things, tech and startups.

* And then those companies invent things that make more jobs obsolete, causing unemployment to remain high.

Are my assumptions correct? What breaks the cycle? Or will it spiral out of control until we decide it's time to stop worrying about unemployment and just start paying everyone a basic income?

Partially correct. Technology companies fall into three main categories:

1.) Companies that let their customers do what they were already doing, but more efficiently, such that they need less manpower. Eg. self-checkout machines, manufacturing robotics, enterprise IT, backend logistics, data warehousing.

2.) Companies that let previously unskilled groups perform the jobs of skilled workers. Eg. EBay (disrupts auction-houses and collectibles), blogging (disrupts the publishing industry), AirBnB (disrupts hotels & hostels), Uber (disrupts taxicabs), StackOverflow (disrupts IT consultants).

3.) Companies that let people perform entirely new things that they couldn't do before. Eg. Google (researching topics that would've been prohibitively expensive to learn about), Kickstarter (funding creative projects), PayPal/Square (accepting payment as a small independent vendor).

The uses of a transformative technology tend to progress from 1 to 2 to 3, because that is the rough order of obviousness and risk to the entrepreneur. When a new technology comes out, all you need is familiarity with the technology and with existing processes to understand where a manual process could be automated outright. This is the domain of enterprise startups founded by people with deep knowledge of an industry and a keen interest in new technology.

Once those opportunities have been picked clean, entrepreneurs look for cases where they could use technology to let a disenfranchised group do the work of an enfranchised group. They take the people who have been rendered out of work in stage 1, and then give them the tools to put higher-skilled workers out of work in stage 2. Doing this requires a strong understanding of both the processes of the industry that will be cannibalized, and an understanding of the capabilities of the workers that will take their job, and an understanding of the technology that lets you bridge the former and the latter. So entrepreneurs here need to do a lot of synthesis and need a bit of "in the right place at the right time" as well.

Once those opportunities are picked clean, then entrepreneurs start looking for things that people want to do but currently can't because they lack the means. This is where the great consumer companies of the next age are formed. It's very risky business for the entrepreneur, though, because there is essentially zero data available on what things people would like to do if they could but can't currently. Usually entrepreneurs that succeed here do so via vision, creativity, and a good sense of what they themselves want to do.

We're currently just starting stage 2 in the Internet/mobile/cloud revolution, so I would expect more job destruction and more short-term social pain in the near term. But it stops when all the easy opportunities of stage 1 and stage 2 have been picked clean, and people are forced to hunt for consumer business models that employ all the people put out of work by the earlier stages. Stage 1 and 2 destroy jobs, but stage 3 creates them.

BTW, for the last major economic transition (the Gilded Age and Industrial Revolution), the stages looked like this:

1. Sailors => Steamboats. Weavers => power looms. Blacksmiths => Steelmaking. Coachmen => Railroads. Miners => bulldozers, excavators, and heavy equipment. Domestic servants => home appliances.

3. Electricity. Home appliances (part of this industry replaced domestic servants, but part let consumers do genuinely new things, like microwaves and blenders). Penicillin. Air conditioning. Airliners. Elevators. Refrigerators. Computers (kicking off the next revolution).

Note that there's a large overlap between the stages. The last stage 1 business, replacing domestic servants with vacuum cleaners and washing machines, didn't happen until after WW2, while the first stage 3 business, electricity, happened in the late 19th century. I think we've seen the same thing with the Internet age, where Google and PayPal were among the first Stage 3 businesses, but Stage 2 hadn't even happened yet.

The general pattern is based on who're the substitutes for each industry. Stage 1 substitutes machines for labor. Stage 2 substitutes labor for labor with the help of machines to do things more efficiently. Stage 3 uses machines (built by labor) to solve unfulfilled human desires.

> stop worrying about unemployment and just start paying everyone a basic income?

What I've never understood about BI is how it works for the middle class. Consider: a cohabiting couple each work entry-level tech jobs and bring in a combined $100k. They buy a condo together, maybe a couple of halfway decent cars. They're being responsible. Then, economy tanks/tech bubble bursts/etc and they have to live off their BI which if I understand correctly should fall somewhere in the $15k/year range each, so $30k total. How do they pay their bills?

In other words, what good is $15k/year when you've been living on $15k/month? Or $7k or $5k/month? It's better than a poke in the butt with a sharp stick, but it's just delaying the inevitable, isn't it?

If then BI is instead mainly for the low-income portion of society, well, we already have that -- it's called welfare/social security/disability. I'm missing something.

I think the point of BI is to keep you from starving. The idea is that no matter who you are or what your station is in society, you should be able to afford food, a roof over your head, and basic medical care. It's not to maintain your social standing in life - someone who has a job will rightfully have a higher standard of living than someone who doesn't. And you shouldn't expect it to be a comfortable middle class existence, you should expect it to involve living like the working poor today - a cramped apartment, not much in luxuries, public transportation or long commutes.

But it takes the stress out of simply existing. The idea is that it's set at a level where you're not going to die, you're not going to end up homeless, you're just not going to be very comfortable.

As for how it's different from welfare/social security/disability - I usually see it pitched as a way of unifying all of those (and the EITC), so that people don't fall through the cracks because they don't know how to sign up or what they're entitled to. It'd save on administration costs as well.

If BI happens, there will be an entire art form developed on how to live happily on $15k/adult/year. This is already taking place (e.g. Mr. Money Mustache lives a comfortable middle-class livestyle with his wife and son on $27k/year).

The other main benefit of BI over the current patchwork of welfare programs is that it removes the disincentive to work on the margin. Today, many unskilled people stand to lose money by getting a job, because the value of their labor is so low that the loss of benefits they'd trigger by becoming employed would actually be more significant than the amount of money they'd make from any job for which they can actually qualify.

This is a stupid state of affairs, because: (1) it wastes the potential labor of such people (which is, after all, generally worth something); (2) it robs them of the psychological benefits of being gainfully employed; and (3) it disincentivizes them from gaining the practice in work and thereby developing the skills that would allow them to get better jobs in the future.

BI fixes these problems by making sure that everyone, even at the bottom, sees positive economic return for their labor.

From a social dynamics standpoint, I suspect that over the long run, this feature is probably even more valuable than the "keep you from starving" features of BI.

Critically, excellent education has to be included in that as well. It's not enough to just take care of bodily needs -- you have to provide a way up, too.

Not an American, but from what I understand from hearing this argument here multiple times...

1. It is cheaper to just hand over USD$1K per month to anyone that bothers to show up at the BI office than to support an army of social workers and bureaucrats to sort out who's worthy of welfare and who's just lazy.

2. It is more fair to just hand over USD$1K of BI to anyone who asks because bureaucrats are not quite good at sorting out who's worthy anyways. Under current system people with genuine dire needs fall through the cracks while the benefits of welfare goes to those who take the time to learn and game the system.

3. BI is in the long term more productive for the whole economy because it can be used to complement/subsidize low income for unskilled workers, while welfare eligibility rules prevent receivers from bootstrapping out of poverty if they cannot find entry level jobs that pay at least as much as what multiple welfare programs already provide.

> It is cheaper to just hand over USD$1K per month to anyone that bothers to show up at the BI office than to support an army of social workers and bureaucrats

Your worst case scenario under this program is 300,000,000 Americans showing up during a downturn in the economy. That's $300 billion a month, $3.6 trillion a year, or roughly 100% of current US budget expenditure (with entitlement, defense, discretionary, etc.)

http://en.wikipedia.org/wiki/United_States_federal_budget#Ma...

So it's definitely not cheaper, even when you account for the cost of maintaining the bureaucracy.

US government expenditure is more than $6.3 trillion. The $3.6 trillion you quoted is just federal spending, and does not include state and local spending:

So, it's more like 50-something percent, not 100%. Also, some of the money would come back as sales tax etc., so the real impact would be less than 50%.

At the height of the great depression only ~23% of workers were out of jobs. That's hardly 100% during a "downturn." At 100% unemployment do you really think our current system of privately owned property would fare any better? Personally I think at 100% unemployment the masses would seize all the property, and probably rightfully so.

So are you inserting a qualification for being unemployed and no longer allowing just anybody to walk in and demand their share of basic income?

Then you're back to the problem of needing to hire more bureaucracy with respective office leases, equipment, etc., to verify the employment status.

Unemployment is also a weak estimate, what you want is unemployment + the negative labor force participation - kids and retirees are not unemployed in the sense that they're actively seeking employment, but would probably not pass up an opportunity for free cash.

> In other words, what good is $15k/year when you've been living on $15k/month? Or $7k or $5k/month?

Not much I guess, but if they're suddenly faced with the prospect of existing on $0/year, I imagine it'd look pretty nice. Quite a lot of people live on 15K per person in the family, so I don't think they'd be hopeless. I think BI is supposed to hit a sweet spot akin to the "better than a sharp stick" thing you mention. You could live off it if you really wanted to, but it'd kind of suck, and your life overall would be more enjoyable with a job.

I think a lot of the appeal of BI comes from two ideas. One: automation technology possibly introducing a "new normal" in terms of unemployment levels, in which case BI might help a society not eat itself. Two: it may, possibly, be much more efficient than the various welfare programs you mention. I don't think that's been proven, but it's a tantalizing idea.

I'm not really an expert on the idea though, so, two cents.

edit - I'm also not sure that automation tech introducing sweeping society-damning joblessness is something that will ever actually happen.

1) even if a basic income disproportionately helps the otherwise low-income part of society, it seems more "fair". Instead of calling it welfare or charity, with the implication that those who receive it are living off the backs of others, and are themselves lazy, it's just something everyone receives.

2) If the hypothetical couple's total expenses are $15k/month, and they can't gear down their lifestyle to $5k/month before running out of savings, I'd propose they weren't really living responsibly. $5k/month is enough to subsist, albiet not luxuriously, in pretty much any part of the U.S.

The alternative is going from $15k/mo. to $0/mo. That extra $5k could either keep a family solvent.

3) even if it merely delays the inevitable, that might be good enough. If expenses are absolutely fixed, but if a basic income allows a person 12 months to find/create a new job in a rough economy, instead of 6, or 3 or none, that's likely to be a success.

What do you see as the inevitable? It wouldn't prevent them from losing something, but it would be the difference between the bottom being living under a bridge completely destitute and living in a shabby apartment until they got back on their feet.

As far as the low-income side of things, the safety nets you mention definitely help many people, but in the US at least there are still many other people who do not qualify for existing programs, but are still very much in need:

- Long-term unemployment - unemployment pay, even with the recent extensions, is limited in duration. A portion of such people might qualify just fine for disability (SSDI, SSI), but many long-term unemployed do not. To qualify a person can't just prove they haven't been able to find any available jobs they're capable of doing, but prove that there isn't any possible job at all they could do, regardless of openings or likelihood of being hired.

There is disability fraud that goes on (cases that don't meet the legal definition, but are misrepresented and approved), especially for areas with very high unemployment, but this is illegal and not supposed to happen, and efforts are constantly underway to crack down, often to the detriment of many unequivocally legitimate (by legal definition) disability recipients.

- For food assistance, the Supplemental Nutrition Assistance Program (SNAP), provides usually $100-$300 per person in monthly supplemental assistance for purchasing groceries. But for those people without additional income to put towards food, it is often not enough and seeking out additional non-governmental help is necessary to not go hungry. In many states long-term unemployed people, regardless of need, do not even qualify (assistance is time-limited).

- Except in the case of low-income parents, cash assistance is very rare or nonexistent most places in the US.

- Health care - the Affordable Care Act (ACA) improved the situation for a large portion of uninsured Americans, mostly by providing variable subsidies for a wide range of incomes, and disallowing insurance companies from denying or cancelling coverage for medical reasons.

Even now though, in some states many low income-people still cannot obtain insurance; some State governments (like Texas, Florida and others) chose not to expand their Medicaid programs to cover all adults below the poverty level, as was expected. In those states non-disabled adults below the poverty level do not qualify for Medicaid, or even for the same subsidies provided to those in higher income brackets.

-----

A basic income would ease a lot of pains for low-income individuals who do not qualify for current aid programs, or qualify but do not receive benefits for various other reasons: like not knowing it's available, daunting paperwork and proof of identity/need requirements, stigma, etc. The bureaucratic overhead of processing applications and managing current cases for a range of programs would be greatly reduced too.

What breaks the cycle is that eventually someone uses all this capital to found a business making use of all these unemployed people. They're an untapped resource.

You're basically describing technological progress, but there's no reason to assume that tech will always replace expensive laborers with relatively smaller amounts of automation. All that productivity created by new technology represents increased demand, and having workers go idle is just as much an inefficiency as using an older process. An inefficiency that can be (profitably) corrected with the right business model.

Tech can, for instance,replace expensive components with cheaper labor (think usability inventions), or help scale up existing production to meet greater demand (think bigger factories). Both of these require more workers in the aggregate, not less.

A lowering of the real rate of interest, either by a voluntary decrease in spending and a corresponding increase in savings, or by an artificial rate set by central bank policy, will indeed lead to more investment into earlier stage production areas such as farming, mining and startups.

Taxes discourage investment, however, so they can change time preference again towards less savings and more later stage consumption. Then again, also here we see a political preference for the early stage production areas, e.g. farming subsidies.

>And then those companies invent things that make more jobs obsolete, causing unemployment to remain high.

I would say this one is incorrect. It isn't so simple as that. Inventing new tech often creates new jobs. As an example look at the different medical imaging technologies created over the years: x-ray, ultrasound, CAT scan, MRI, etc. Each added to the number of medical imaging jobs it didn't obsolete anyone.

You should check out some Karl Marx sometime. This isn't exactly what he says, but it is a part of it. The concepts you refer to in your post are called "fixed capital" and "variable capital" and their ratios, as well as the "reserve army of labor," amongst other things.

I haven't seen any evidence that suggests starting a company during a boom economy makes it easier to succeed. It does make it easier to get a salary while failing though (which is better than just failing and getting nothing).

What will this all means in terms of "smart" angel money versus "dumb" angel money? If angel investing is becoming more a matter of prestige than thrill/returns, it could become much easier to get an angel round, but at the price of dumb investors who lack the patience or stomach to deal with the ups and downs of startups.

I know I'm going to have to look for angel money in the next year. And when I find my angels, I want them to be the first people I turn to when things are hard. I want them to be genuinely helpful and supportive, not angrily demanding to get their money back at every little hiccup.

We decided not to pursue subsequent rounds of funding beyond a seed. I'm also hearing about deals with quite cheap capital (high valuations, favorable terms) flowing to companies near us.

For SaaS it seems you can get deals with valuations at 10x revenue and YC Companies in SaaS are getting a premium even on that.

Cheap money can help you weather a storm and smooth over mistakes, but it also increases your risks as a business and reduces the "successful" outcomes you can have.

At the end of the day if your goal is to build a sustainable business, cheap money can't guarantee that.

I don't know what this article was trying to convey.

Valuations are a subjective airy-fairy number and, in reality, based on the strategic need of a buying entity. For example, when I was in the process of selling my last business I had 3 offers. 2 offers were from companies that wanted me obviously but didn't need me strategically, therefore their valuations were low. The 3rd offer was from a company who had a hole in their product-line and my tools fit perfectly in that hole, hence their perception of my company's value was much higher.

So find businesses which have a strategic need (or convince them of such need). Also, I would assume but have no evidence that strategic acquisitions have a higher success ratio than purely financial acquisitions.

And just like salespeople should 'always be closing', business owners should 'always be exiting'.

> And just like salespeople should 'always be closing', business owners should 'always be exiting'.

That's interesting, could you expand on that a bit? Do you mean you should always have a few good exit scenarios prepared (e.g. keep a few potential acquirers interested) in case you need one?

Sure. A business should always be prepared for outside interest meaning that you should have up-to-date financials that you can give-out anytime which show the summary information and overall financial trend, have no unusual liabilities like a unpaid tax liability, systems in-place to automate business functions (so a potential acquirer can see an efficient organisation), all employees/customers on some kind-of contract, no IP issues (all B2B relationships under contract).

So any business with interest can spend a minimal time in due-diligence and see an efficient, professional organisation with no skeletons.

At the same time, the goal of business is to exit, either via a buyout, or IPO, or whatever. No one wants to own a business that is unattractive for acquisition or investment, since these businesses just fade-away over time.

So the directors need to continually look for potential strategic relationships; a) because these are obviously potential customers, and b) because they are potential acquirers who will pay top-dollar for your business. This means that they will forget any standard valuation formulas ('X' x sales, 'Y' x EBITDA, whatever) and look at their overall strategic need for what your business will bring to them. And, most importantly, you need to communicate with them on this strategic level... so you need to do your research and keep your ears open to understand their pain points, and strategic needs.

By keeping your house in order, looking at the strategic level, and trying to elicit the interest of those businesses who 'need' you, you may get yourself in the perfect situations where you have competing bids, or the interested parties start to think (with your gentle prodding, of course) of the pain if you were bought-out by their competitor, etc. These are the ideal situations. But they don't happen by themselves, hence my line: always be exiting.

I recently took a trip to Asia where capital is hard to come by and startup valuations are much lower. It seems that if VCs are having trouble finding return, they might be well served by investing in global expertise.

Are the consumer markets so much better in America that it's worth paying 4x valuation and competing with lots of other VCs for deals? The answer may be "yes", but it doesn't seem obvious to me.

> Are the consumer markets so much better in America that

> it's worth paying 4x valuation and competing with lots of

> other VCs for deals? The answer may be "yes", but it

> doesn't seem obvious to me

Don't forget that there are known quantities of legal/tax vehicles for VC investment in certain countries. If those things are not present, I imagine it would increase the risk for the VC, and impact valuation and capital availability.

Don't forget political risk. Rundown of Asian countries with political risk comparable to the US; Japan, Lorraine, Taiwan, Singapore. Countries with more political risk but not much; India, Indonesia, Malaysia, Thailand. The second group have much worse legal/regulatory systems for doing business. I wouldn't plan on getting incredibly rich in any other Asian country unless I had a friend/patron to protect me from expropriation/gangsters. And you better be able to provide your friend with some quid quo pro orbe related tl them either by blood or by kid.

I may be overly cynical here but that's the perspective from China.

The consumer markets and VC climates in other markets can be much worse. Take china for example...the VCs are only interested in funding shanzhai rip-off copies of ideas of ideas already proven in western markers.

Probably not all that different from the last one. Economy starts heating up, and the Fed begins to tighten interest rates to damp down inflation. It takes time for interest rate hikes to make their way through the economy, so they keep tightening. Eventually, everybody realizes that money isn't cheap anymore, and moreover, they realize that everybody else has realized that money isn't cheap anymore. That causes a mass stampede for the exits as people fly away from risk.

In the last crash, the economy started heating up in 2004, the Fed started tightening in 2005 and continued through 2006, the market hit a top in August of 2007, there was a slow-motion recession through late 2007 and early 2008, and then everybody ran for the exits in the summer of 2008.

This time, I think the economy started heating up in 2013, the Fed is planning to tighten starting early 2015, it'll take about 18 months for the rate hikes to make their way through the economy, and so I'd expect a crash around 2017.

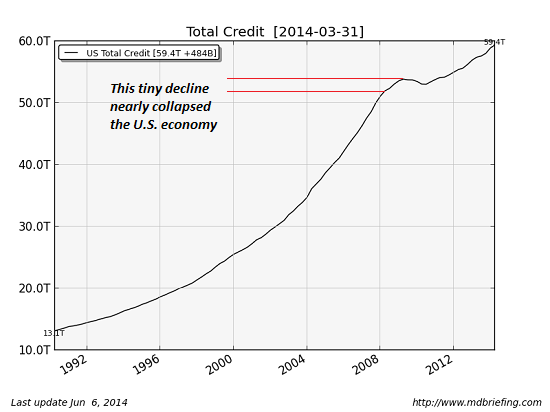

We are in a debt bubble propped up by massive central bank intervention all over the world. The intervention will fail at some point and well get a bout of deflation just like in 2008, only this time more severe.

We’re more and more A rounds happen with less than 20%

ownership going to the investors, and fewer and fewer

requirements about investor control over the company.

{kind=link}

{kind=link}

This is very interesting. If ownership percentages at Series A are trending down, and investor time & emotional investment per company is trending down as a result, but having outside accountability predicts success, then I wonder how the best companies will replicate outside accountability.

Put another way: How could you hack a replacement for a board meeting?

I'm a funded entrepreneur without a board. I've tried nominating advisors and/or very-helpful angels as our "pseudo-board" and meeting monthly. This didn't help very much: There's something about having a lot of skin in the game that makes board members really prepare, take it seriously, and summon courage to have hard conversations with CEOs when things aren't working.

The one thing that worked pretty well was bolting a whiteboard over the desk area with this month's single goal (a revenue number, natch) and value so far. I don't have any board experience to compare it to, but it certainly keeps us focused.

Anyone else have ideas that have worked, or might work?