So from Buffett's perspective this just looks like a bond. I don't think it's a bet for or against solar, but rather a bet on deferred cash vs present cash (so on interest rates).

I wasn't expecting this comment in Hacker News. I can only agree. Indeed, this is an investment with a risk/return profile of a utility, not the technology.

The telling point, and why this is on HN, is the important threshold that a seasoned investor can buy solar to make money for the purpose of making money.

It seems a fair argument until you notice that oil is subsidized too though the relationship of these subsidies and how they compete with eachother is complicated and not worth debating.

If anyone wants to learn more about how this stuff works (and why does Buffett does these types of deals), then read the book Security Analysis by Benjamin Graham.

Yes, they have shifted from pure number crunching (which is Graham's approach) to a system that values future growth potential more. In Graham's style you can only judge a company on its past dealings, cash in hand, inventory, equipment, etc. But Buffett knows that companies also have other qualities that are very valuable, but not commonly considered as such. He went from a pure quantitative approach to one that is quantitative and qualitative. Hence, when he talks about moats, he is talking about those qualities that you cannot price, but are still very valuable. One great example of this is his investment in Coca-Cola. Not a great investment in terms of financials (dont get me wrong, it makes him money) only, but also in terms of all the goodwill that the Coca-Cola company enjoys (they invented Santa Claus!). So investing in it made sense because their long term prospects were positive given the past history and goodwill status.

Coca-Cola is seen to have invented what Santa Claus is today - mainly through helping to change public consciousness of him. They did so initially through Haddon Sundblom’s depiction of him for The Coca-Cola Company’s Christmas advertising in the 1930s[1][2][3] & he is constantly used in their campaigns at Christmas.

My friends etc always say "It's not Christmas until you see the Coke ad" in reference to the build up to Christmas.

However, they weren't the first company to do so as in 1915 and 1923, White Rock Beverages used a today's version of Santa (Red & White) to sell mineral water and ginger ale respectively.[4]

No, they didn't. I am on an android and having trouble searching. But they apparently popularized a particular image of Santa. Off the top of my head, Santa is originally based on a real person but the modern image doesn't much resemble Saint Nicholas of actual history. Modern commercialization has had a huge impact on Christmas and pushed gift giving over more traditional spiritual celebrations and, iirc, modern commerce invented Rudolph the red nosed reindeer (though I think it was a different company, not coke).

Google it yourself. You probably are in a better position to verify it than I am, with my wonky android browser freezing up and saying "bite me, bitch" on a regular basis.

You are correct, and I stand corrected. They didn't invent it, they just made it what we today know as Santa Claus. In other news, Pepsi is known to have invented festivus. News at 11. :)

Santa already had a red coat with white trimming - at some unspecified point in the past he did have a green coat.

Coke took an already-popular meme with no trademark and co-opted it for their own marketing, popularising it even further. The expansion of the Coke-themed Santa led to the belief that they invented it.

Something to absorb for those who are trying to work out how to market things.

I know all this because up until 10 days ago I also thought that Coke invented Santa, until I realised I should fact-check that, and found out I was wrong.

He's betting that they'll stay lowish, or at least lower than whatever return he's getting here (not enough information in the article to tell). If you treat this investment, in return for a 20-year guaranteed rate, as sort of like a 20-year bond, it shares the characteristics of long-term bonds that you're betting against any unexpected increase in interest rates. If interest rates increase more than was priced in at the beginning, e.g. there's a big rate spike in 2017, then you would've been better off keeping your money in short-term bonds where you can take advantage of any upwards movements, rather than locking in a fixed return for 20 years.

Agree to your comment, but all PPAs I've seen/been part off, are indexed/hedged to CPI/energy CPI and/or oil & gas prices. It would be irresponsible for whomever negotiated and valued the PPA not to factor these.

No PPA without this type of hedge/terms is financeable - today more than ever.

Are the terms of these contracts public information? And if so, can that be used to give us an understanding of what "interest rate" Warren Buffet is getting on his purchase?

Unfortunately they almost always are. The utilities are in the enviable position of buying wholesale power from renewable generators on 20 to 25 year fixed price, flat contracts. Of course they would never agree to sell power to the customers on the same terms - which is why it is great being a utility!

I can only speak to California utilities, but in CA, by law, utilities are permitted to earn 11% return on capital. As there is no customer choice when it comes to electric power (you only have one provider running a wire to your home), the utilities simply get the rate approved that they need to generate the allowable return. So prices don't "fall", because the utility is constantly investing in new assets (generation, transmission, smart meters, new power purchase agreements) raising their capital base and thus either sustaining or raising the rates (price) to consumers.

Am a huge follower of Charlie Munger, and I re-read his writings every so often ( http://www.tilsonfunds.com/motley_berkshire_charlie_speeches... ). What the two of them do is so much of a one-trick pony. They always seek massive rent capture via outright purchase of a corp with a very large moat. Then reduce the fiat risk by converting the cash into non-fiat income producing assets. This way they lock in wealth preservation regardless of what happens to the fiat. When I lived in New Mexico for a bunch of years, there was one constant - the incessant back and forth of the trains carrying coal containers from one end of the country to the other, and on the return trip carrying giant walmart containers shipped from China to the US ports, to their destinations in the rest of the mainland US. Everybody knew BNSF was the coronary artery of the US. One day I remarked to my wife - just you watch, Buffett is going to own BNSF. And then when it happened, she was like - how did you know ?! Its just so obvious. This SunPower thing was on the cards too. Prediction: He'll buy Vestas. Or Nordex. Just you watch...ofcourse you can't time these trades. Nobody knows the when, but the what is fairly well known at this point.

The way I understand what dxbydy has been writing, he or she is explaining how Warren Buffett often plays the opposite of a venture capitalist, risk-wise. He isn't a futurist, he picks off clear winners who are firmly entrenched in their markets.

While this is always a tough strategy -- because the easier they are to find, the more likely these companies are to become overrated -- it gets a little easier when you have a massive amount of capital. It's still tough to do consistently though.

The term "Rent Capture" calls out the distinction between entrepreneurs and landlords. The worth of land is obvious and so it takes other competitive advantages besides ingenuity to close a big deal. Pejoratively, as dxbydy mentioned, "rent capture" implies that the owners don't have to work very hard for their money.

"a very large moat" refers to the barriers to entry. Imagine you have 4 or five companies who built power plants 40 years ago. It was expensive for them at the time, but they made back their initial investment years ago and now the only thing they care about is market share. The size of their moat is proportional to how much it would cost for some new company to build their own power plant.

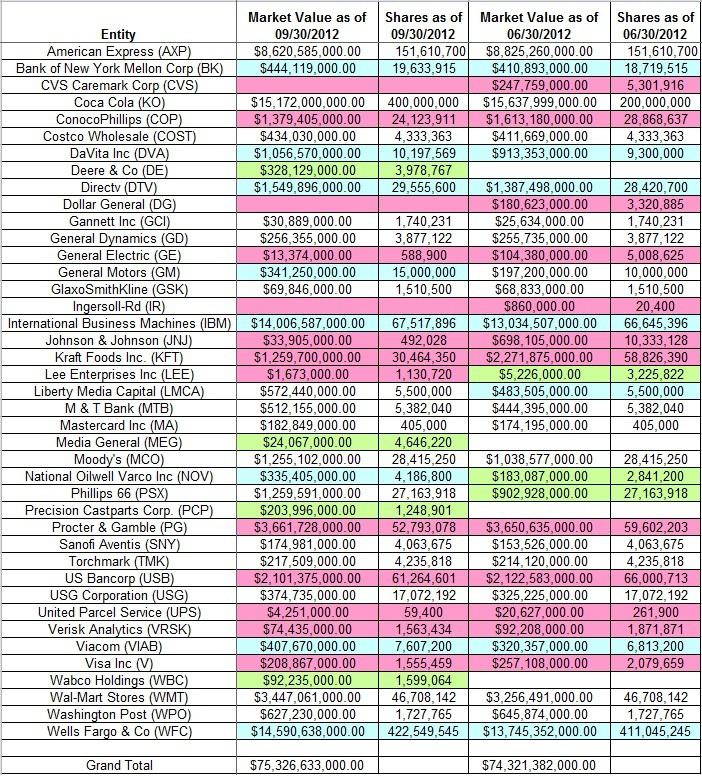

I think you do :) Probably you disagree with the characterization. I don't see why rent capture generally has such a negative connotation outside of finance circles. Its a perfectly legitimate strategy. And who has a larger moat than BNSF or Vestas or SunPower ? Even if you were a Zuckerberg you couldn't build these things in decades. Takes forever just to buy the land, spec out these things & get the specs approved by regulatory bodies. So if you could buy these concerns outright, you would. You would buy, whether it was making solar power or your underwear. ( He owns the largest underwear maker Fruit of the Loom ). Given the asymmetric info advantage he has, he's sold millions of puts expiring in 2019 & is sitting on top of billions in premium ( while simultaneously telling the American public that derivatives are instruments of the devil :) Got to park those assets someplace, otherwise fiat risks accumulate. His stock purchases for 2012 are quite ho-hum...utilities, banks, big media ( http://static.cdn-seekingalpha.com/uploads/2012/12/4/sauploa... )

> I don't see why rent capture generally has such a negative connotation outside of finance circles.

Well, it violates a lot of views of how the market "should" operate, on both the left and the right. On the right, some simplified versions of free-market views assume relatively perfect, efficient markets will normally develop absent government distortion, so they're suspicious of areas where rent is being extracted as probably due to some kind of intervention preventing a proper free market from operating. And on the left, many see rent-extraction as a paradigmatic example of the power of capital relative to labor (the ability of passive rent-extractors to in effect collect a "tax" from active economic activity).

people who do not own "rent producing assets" have a bias towards those who do, because a "rent producing asset" is something that gives the owner money, without the owner producing value, other than making the asset available. It is basically a facet of jealousy if you ask me...

Whether or not Tycho understands your terminology or not, I don't, and I bet a whole bunch of people don't. You use a lot of jargon (not in the negative sense of the word, but in the sense meaning highly specialized vocabulary). Could you actually answer tycho's request?

I hate to dumb down stuff that even wikipedia takes 2000+ words to summarize. But simplistically, Buffet is sitting on a mountain of cash. If interest rates go the wrong way, he is exposed to fiat risk. So his best bet is to trade that fiat risk for non-fiat income producing assets. He does that by outright purchases of very large companies whose competitive advantage is so huge they'd be impossible to defeat, and yet you can't get by without them. I mean, what are you going to do if you want 1000s of giant walmart containers sitting in LA moved to the midwest, and you don't like BNSF's pricing ? You are essentially fucked. So you play ball with BNSF. That's your moat right there. You can't build a railroad, not in today's climate. Its not like a gmail or an oracle in that you think those companies suck, so you switch to hushmail and mongodb. You basically have an out, so there's arguably no real moat in technology. But with large scale infrastructure projects, once you own a piece of them, you can just sit back & collect rent & everybody has no recourse other than to pay up.

"If you can't explain it to a six year old, you don't understand it well enough yourself." -- Einstein

In other words, express your command of a subject by how simple you make it appear, not by demonstrating how impressive and complicated the subject is.

I remind myself of this concept routinely, and struggle to reflect it in my writing and peer communications.

Thanks for the dumbed down explanation. I had a very clear idea of what you meant from your first post, however, the extra clarity gives me confidence that I understood it correctly.

Your first comment also dumbed down the exact same material - but in a different way. In the present day, among computer users and maybe people interested in finance, I have noticed the use of terser expressions, dense walls of text and shorter words to approximate the meaning of longer concepts (e.g. "moat", "sticky") to avoid recreating 2000+ word wikipedia articles.

Your first comment and the earlier commenter suggesting 'coca cola' having 'invented' santa claus (the user didn't mean the dictionary definition of invented), where two people are using language that has moved on from the dictionary definition, reminds me in some way of this essay by George Orwell.

I prefer the present-day contracting "meaning concentrating" style of abuse of language rather than the olden-day expanding "meaning dilution" style of abuse, however both make for uncertain reading!

I don't agree that Rent Capture is the correct terminology, because Buffett isn't using political or social engineering (so to speak), in order to capture the market.

He is simply finding companies with very high switching barriers that have occurred naturally in the market.

We usually associate "Rent Capture" with activities like limiting the amount of taxi licenses in a given city which helps incumbents but drives out competitors.

I don't see SunPower as being like the others. It's very, very hard to build a new set of railroad tracks so a railroad is pretty much of a monopoly. Anyone can (and does) build solar plants. It just takes capital and patience. Also railroads (and utilities) have immense lobbying capabilities and so are able to get very sweet, ever increasing rates (although for railroads they do of course have to compete with other modes of transport, but I'm sure with rising fuel prices they have huge advantages compared to over the road). SunPower however, as a developer, has to SELL to utilities and have NO pricing power nor real competitive advantage. They also typically sell on long term fixed price contracts in order to obtain financing and because that's typically all the utilities offer. I would be interested to know if Buffet has some kind of swap or other financial product that trades the long term fixed price stability of the investment (although low yielding) for something that provides more yield but is more variable.

With respect to "rent capture", they're referring to economic rent. Basically, a situation where competition cannot affect the price of a good. Great if you receive payment for that good, less so if you're paying it.

Pretty sure "moat" is a term popularized by Warren Buffet himself to describe a company with some kind of inherent advantage over it's competitors. As in, when a company with a moat succeeds, his competitors have a hard time entering that market and replicating that success because of the moat.

A moat protects your marketshare. A very large moat then would be, I guess (I'm not an investor or anything), a company with a large competitive advantage and a market share that would be very difficult to steal.

A good example of a moat - and a company that Buffett has invested in - Coca Cola.

They've invested enormous sums in marketing sugary syrup, a product with a sizable margin. Others produce sugary, fizzy water too, but there's only one Coca Cola and it's impossible to overcome in the marketplace.

Rent capture: landlords collect rent on the house they own the right to. Similarly, lets say the government or any contracts grants some body special privileges, the money they earn on those privileges in excess of what they would have otherwise is a rent capture. EG: lawyers get more money because only they are allowed to do certain legal work. The rate they collect in excess of what someone unlicensed but qualified would charge is a rent capture (rent seeking activity?[0]).

fiat (govt currency) risk is if you are keeping 100 million in a bank account and Bernanke keeps running the printer, then one day you will wake up and it will buy approx three eggs.

So best to ensure you have physical wealth assets on hand that can't be conjured out of thin air.

What about FDIC bank guarantees? Well sure the 100 million is guaranteed. It's purchasing power is not.

it sucks that purchasing power is lost for people without lots of money. It seems inherently an unfair system - if you stop producing value, your existing store of value diminishes thru no fault of your own.

the trick is to realise that currency was not designed to be a store of value so don't use it as such.

To paraphrase Silvio Gesell, an economist in favor of symbolic currency almost a century ago, "All the physical assets of the world are at the disposal of those who wish to save, so why should they make their savings in the form of money? Money was not made to be saved!"

ie: you don't need to buy whole companies outright to avoid saving in currency.

I am presuming that the moat being in this case the high locked in prices paid for solar power at the peak of the 'we must create renewable energy' frenzy.

It is unlikely that new solar plants would be able to get the same types of long-term power supply contracts that an existing plant might have got 5 years ago. At the residential level, most solar FIT have been slashed as government programs ran out of money and public enthusiasm waned as the non-participants bills went up.

But yes, a solar power plant is a utility, and if it has locked in contracts (I admit I have no idea if it does) it would be a good buy, if nothing else but for the inflation hedging as power always follows inflation but many other revenue streams do not.

They might also enjoy from tax breaks (future or present). I'm not clear on how, but with Buffetts talent to bend tax laws, you can be sure that is taken into account.

I always wondered if it would be possible to create a fund or something that invested/bought up bankrupt but useful infrastructure projects. The two that spring to mind our Iridium Satellite Phone and the UK-France Channel Tunnel.

Both excellent ideas that were unlikely to earn back the cost to produce them, but if bought after bankruptcy and sunk costs have been written off they could be profitable.

I have a feeling that this is not an investment to Buffet, but rather a means for him to influence the market. People now follow his investments religiously, and an investment like this in to solar could spur a lot of people to make similar capital investments.

In effect, Buffet is now making a demand for green companies for copy-cat investors to invest in.

He is incredibly passionate about capitalism. Especially smart capitalists responding to pricing signals intelligently. And the symbiosis of good management and good investors to keep companies efficient, take smart risks, and earn consistent, healthy returns.

Making huge, counter-intuitive investments is nothing new for Buffett. (Railroads anyone?) I imagine he is doing this for the reason he usually does: he thinks he is getting a huge amount of value for a low price.

If by "not an investment", you mean that he doesn't believe that it will throw off more net-present value cash than a similar investment in the S&P, then I strongly disagree.

He may think that it would not have done that without his investment -- so it could be both, but Buffet promises investors that cash will be deployed more efficiently than you could by just buying an S&P index fund.

I don't think this isn't an investment, but I think there were motivations beyond purely investment; and having heard him speak and read what he has written, I am taking a guess that he was motivated out of an idea to influence good (while still making a sound investment).

Nope. The tax incentives go to the investor involved in building the project and are usually captured by a bank that trades the tax credit for an equity investment which lasts for about 5 years (the minimum period to avoid recapture).

This is most likely a tax play. Renewable energy projects are almost always financed through tax incentives that can be used to offset tax liabilities elsewhere. Could be seen as hypocritical of Buffet considering his recent musings that rich people should pay their fair share. Here he is trying to avoid taxes.

First of all, he's not personally buying it, so it's not like this would reduce his personal taxes. Secondly, your first sentence is clearly speculative, but then you act as if it's definitely true for the rest of your comment - do you have any evidence for this whatsoever?

You are correct. Berkshire Hathaway would benefit, not him personally. The tax credits are a big reason these things get built. There is a 30% solar tax credit that can be passed through to owners against other income.

The reason this may not be a tax play for him is that ConEdison or SunPower may have already stripped the tax credits from the project and sold them independently. This means there may only be a long term investment vehicle that insurance-type companies like to hold. But someone benefited from the tax credits and I wouldn't be surprised if they were part of the deal.

According to your link, the tax credit is only available to the original installer of the solar facility, i.e., the solar plant in this case. In order to take advantage of the creditk, the solar plant company would have to file a consolidated return with Berkshire Hathaway.

I don't think it is because Buffet is all about making long term investments. Tax incentives that will go out of fashion at some point (probably in next 10 years) wouldn't impact his decision as much as sound business fundamentals and future potential.

However, even if it is a tax play, it's not inconsistent with his POV that the rich should pay their fair share. You can believe that the rules are currently broken, yet play by the current rules. One is about what you believe to be fair and the latter is about what is in the best interest of your shareholders.

If this is hypocritical, so is paying the lower tax rate than his secretary, even thought he complains about it. Anyone thinking its hypocritical is missing the point. He does it to show it exists. Sure, you can not do it, and donate to the government on your own, but that's not fixing the problem. The small number of donators can't fix the deficit on their own. It takes a law that required everyone to play ball in order to fix the problem.

It will be interesting to see where the energy market will be in the next ten years. I do believe that at some point people will need new forms of energy since the forms we currently have are too expensive (or getting to expensive) for the average person to afford. Since the market needs the majority of people (in the popular cases) to need their energy, maybe it will adapt. I would like to see some more competition in the market of energy; in most small cities in the midwest and some of the larger ones there are virtual monopolies allowed by the cities. This is sad, and I think the business sector can do a lot better. Warren Buffet paying into solar is a promising sign, however I think there needs to be a lot invested in brand new technologies that havent been created yet.

I know I've noticed a boost in the amount of properties that have solar in my area in just the past few years. Solar pool heaters are very common now too.

With companies offering financing for the sell-back programs with solar it's going to improve, I know bungalows in our area that can get a decent sized system installed can make about $2200 a year, pay nothing for the installation of the system, and get tax cuts. Smaller systems are still worth it, you're just not going to get many people paying $10,000 up front for a few kilowatt system that'll take 7-8 years to pay back.

I expect as efficiency in systems go up there'll be a huge improvement in the numbers of people with solar. I know with the current systems I can only get a 2-3KW system on my roof (the south facing portion), which isn't worth it with the install costs, etc required for the sell-back programs. In 10 years when the solar panels being sold are close to the efficiency we see in labs today, it will be cost effective for just about every property in a suburban area to get solar systems set up.

We're literally on the precipice of a power revolution. I wouldn't be surprised if we see architecture change to increase the amount of south facing roof to increase the amount of energy properties can get. Imagine when the majority of power for cities is being supplied by the suburbs surrounding them.

Any abundance in electricity will absolutely fuck the natural gas market. I know running an electric furnace in my area costs about 50% more than natural gas, but when home owners are making more money from their solar system than they're consuming, electric furnaces and hot water heaters will break peoples energy expenses even. Paying $0 a month for all your utilities, or even getting paid per month, will change the entire energy market.

> I do believe that at some point people will need new forms of energy since the forms we currently have are too expensive (or getting to expensive) for the average person to afford.

Isn't shale gas actually making energy more affordable at the moment?

This article significantly misconstrues Buffets investment style. He does invest for value. But he doesn't even think whether a stock has "bottomed in the market price". Predicting when a stock has "bottomed" is not possible as it's dependent on the whims of an irrational market.

The first half of this statement is correct and the second half is completely wrong:

"He only buys when he's sure that an asset is undervalued and is likely to have bottomed in market price."

Then you could look at this move as a hedge against rising energy prices, not entirely unlike his purchase of Burlington Northern Santa Fe. Energy prices are, of course, a hard game to predict, with above-average political risk, especially in the renewables arena...

Fixed revenue usually. Actually to be more precise, fixed price, but declining revenue because the production goes down as the panels (and inverters) degrade. Usually assumed to be .5% per year. The contracts with SCE are typically not based on market prices.

1. Investment is a contrarian thing. Else you overpay.

2. If it makes sense now as a profitable, you go for it. He probably pre-sell a lot of the output at fixed prices, or you hedge or whatever. Technology always improves, but future money is worth less than money now.

"If you anticipate technology improving or prices for energy coming down, you wouldn't invest in today's technology."

Why not? The amount of profit he makes is already basically fixed up front, and more generally the amount of profit these investments generate will probably only decrease as the technology improves.

I really really hope that Solar energy takes off and is affordable/feasible enough to be used by consumer households. Yes we still are not quite convinced by it and probably not there yet, but imagine if we did.

This actually fits Buffet's investment model. He tends to purchase only when a company is down or undervalued and then plays the long angle. He's not a trend investor, he invests based on assets and P/E, etc. AKA "Traditional" value investing methods pioneered by his mentor Benjamin Graham.

It goes all along the profit way for buffet. Save TAX , make huge profit , CONTROL (energy, news media, etc) So its not about solar per sè its about profit , most probably Long-Term profit.

{kind=link}

So from Buffett's perspective this just looks like a bond. I don't think it's a bet for or against solar, but rather a bet on deferred cash vs present cash (so on interest rates).