Facebook is heavily (heavily!) reliant on display advertising, all of which is a) challenged by the switch of its userbase to mobile, and b) going to hit critical mass eventually. No matter how smart you make display advertising, there's still a cap on how much you can foist onto users before you piss them off.

IMO, Facebook's future depends on two things:

1) Figuring out how to serve up contextually relevant ads on mobile platforms in a nonintrusive and, ideally, useful way.

2) Figuring out how to serve up contextually relevant ads outside of Facebook, to Facebook Connect-backended partner sites and apps. (Sort of like an AdSense/AdWords hybrid, but based on very intelligent user-interest and browsing data).

I'm betting on #2's being the runaway breadwinner for Facebook in the long run. The longterm strategy seems to be to reduce reliance/dependence on Facebook.com in favor of Facebook Connect.

I've been saying this for a while now (http://news.ycombinator.com/item?id=3041689). Facebook's engagement is shifting to mobile. Their entire business model relies on web. Their app ecosystem has been crashing as a result, and display advertising is likely to follow.

Facebook is filled with smart people. They understand the trends better than we do. As you'll note, 4 of their top 5 Risk Factors relate to the web-to-mobile shift and the problems inherent with that.

From the filing:

#2 - "We generate a substantial majority of our revenue from advertising. The loss of advertisers, or reduction in spending by advertisers with Facebook, could seriously harm our business;"

#3 - "Growth in use of Facebook through our mobile products, where we do not currently display ads, as a substitute for use on personal computers may negatively affect our revenue and financial results;"

#4 - "Facebook user growth and engagement on mobile devices depend upon effective operation with mobile operating systems, networks, and standards that we do not control;"

#5 - "We may not be successful in our efforts to grow and further monetize the Facebook Platform;"

I think this is correct, and it explains why the IPO exit is happening now. Most of the insane growth (in profit as well as valuation) has already been squeezed out.

> "Most of the insane growth (in profit as well as valuation) has already been squeezed out."

I would amend that to say: most of the easy growth has been squeezed out. But there's still a huge opportunity for Facebook to grow revenue/profit if they switch to using personal data to make well-directed ads they can push to sites using Facebook Connect and/or if they can roll out a solid first-party Facebook-phone. [1]

Those are both far trickier than "grow Facebook", so it does make sense to capture some returns now. But I think it would be short sighted to write their future prospects off entirely.

[1] They could quite possibly fork Android and do to Google in the phone market what Amazon is doing to the tablet market. And they'd be crazy not to try.

I would agree with you here. Most of the low-hanging fruit has been plucked. But that doesn't mean the low-hanging fruit is the juiciest. As I mentioned in the grandparent comment, and as I agree with you, Facebook Connect is the future of Facebook. Facebook seems to understand that fact, and now it's just a matter of how keenly it does.

Facebook has (wisely) focused almost entirely on user growth and retention over the last few years. That it stumbled into being an attractive display-advertising platform was almost inevitable, and required little effort. The real money lies on the distributed mobile and web ecosystem, into which Facebook has been diligently inserting itself as a de facto credential and backend. (Think of Facebook as the "Intel Inside" of the entire content web and mobile content web, and you get the idea).

Facebook has established an impressive beachead with FB Connect, and from there, it's only a matter of time before it can monetize its FB Connect partners through contextual and interest-based advertising services. Google should be very concerned -- and, to that end, it would not surprise me in the least if the threat of FB Connect to AdSense (and, to some extent, AdWords) was a significant factor in the race to develop Google+.

It's unlikely that Facebook is trying to time their IPO at the height of their potential. I think they still have a lot of room to grow the display advertising business, but unfortunately there is a shift to mobile and the Facebook mobile UX isn't that great. I think they need to continue to worry about building products users love and improve mobile UX, advertisers will always come to where the users are.

> #4 - "Facebook user growth and engagement on mobile devices depend upon effective operation with mobile operating systems, networks, and standards that we do not control;"

Interesting. While the other points are gloomy-doomy and a bit vague, this one lends itself to a concrete solution, doesn't it?

I like that they point this out, but in theory this goes for the desktop as well. I guess the difference and reliability between the desktop OS/browser platform is seen as more established than the mobile platforms. This makes sense right now, but may well be something that grows over time into less of an issue.

Very cool to see good reach come from that, do you think it resulted in greater attendance/interest? It seems like the ad you ran reached about 20% of the entire Seattle market with those numbers.

I'm wondering, this might seem absolutely ridiculous, but would Facebook not benefit from having their own mobile operating system, even if its based off Android. Services are no longer apps or on the web but part of the system. Phone numbers are obsolete, you would phone facebook contacts as you would on skype. Such a system could perhaps offer better advertising capabilities and offer another competitor against Google and Apple on the mobile landscape..

Let's not get carried away, this is not true at all. Even outside of tech circles, there are plenty of people that have no interest in what Facebook offers.

Thats true, but I think there could be a way around that if we had a domain name service for telephone numbers whereby instead of having to remember a 12-10 digit number with area codes for someone, we only need to remember a word or sentence and since a string (lower alphabet only) is base 26 it might be easier. Also could we not run out of phone numbers anyway like with ipv4?

You could use the same argument to say IP Address are obsolete because of DNS, but I don't think IP addresses or phone numbers are going away any time soon.

IP(v4) addresses are going away though! No one but the network staff will notice.

Semantically, choosing "obsolete" might have been incorrect, but I think the point stands. IP address and phone numbers don't matter anymore to the end users.

A Facebook mobile ad network would be huge. Mobile publishers are already suffering with low eCPMs, so they are hungry for new solutions. Showing brands/banners is one thing, but showing mobile app ads is another.

Since a lot of mobile apps have some type of Facebook integration (ie: a Facebook app id), Facebook has a good idea of who has what apps installed and they can serve up apps that are relevant to the user both on the interest graph and the data of what other mobile apps they have installed.

Wouldn't be surprised to see them move into mobile advertising hard in 2012/2013.

* Disclaimer: This is all speculation, no insider information was divulged

The people will still use the Desktop like before. The problem is, for messaging and status updates is mobile totally sufficient.

They talk much about Pictures, but most of the people i know don't post any. The big success of Facebook is the E-Mail IM replacement for young people, but it is very difficult to advertise on that. Who made ever money on IM and Mail? ICQ and AIM had impressive numbers, but were never a big success financially.

People in your social network may not post pictures, but for all the Facebook users I know, pictures is very critical part of their experience. [I personally don't use Facebook.] Facebook has actually solved the problem of sharing pictures with your loved ones for non technical people, IMHO.

Funny i don't use it myself, i get an email when someone sends me a message.

I know also people who share them, but max every week and probably just 5 friend really look at them. When you look at pictures, how can you concentrate on ads? They are not even in the middle like Youtube's. Pictures on mobile reduces the space for ads even further and you will always be uglier than every competitor.

I do not have any opinion about ads, I was only replying to your comment that no one shares pictures. Since Facebook, all the non technical folks I know have stopped using Flickr/Google Albums/Snapfish/Photobucket/<<Name Your favorite photo sharing Service>>. They also don't send pictures by email. They simply upload it to Facebook.

Ad serving (at least the monetizing part) isn't always about how you can make a user concentrate on an ad. How many free iOS games out there serve up unobtrusive ads that you sometimes even stop noticing?

>They talk much about Pictures, but most of the people i know don't post any.

I'm not really sure that applies universally. The majority of my stream post pics from mobile (either directly, thru instagram, etc.).

>The big success of Facebook is the E-Mail IM replacement for young people...

In mobile? I don't see that happening either, as most too used to texting/iMessage/BBM

Where I do see a lot of usage is in-stream. If they can figure out how to serve up ads within the timeline without being too intrusive then that would be the way to do it in mobile. Tho that new timeline crashes more often than it works in mobile (at least in the iOS version)

Well i am certainly not an expert, but none of your examples get's people to use Facebook on the desktop.

What is the benefit of looking at someones timeline and how often will you do it? Facebook needs incredible engagement (what it has right now on the desktop) and space do display ads. Youtube has the content, but what brings people back to FB? Don't forget all these social Startups will hurt Facebook on engagement.

Sorry, I understood your op as you making the point that people will still use Facebook on the desktop. I was providing the counterpoint that it is looking more and more like mobile is the future.

Also, I believe stats will show that engagement is rising rapidly on mobile, and that's what keep people logged on FB.

And I'm not sure that people who are currently not using computers at all (in emerging markets) will ever use PCs. If you've never used a PC a smartphone might seem like all you'll ever need.

Hmmm. I think the obvious transition would be to ship the Facebook Phone and heavily incorporate Facebook Credits.

The four things people do on phones (call, email, text, and nowadays photo-share) are all inherently social things. Crucially, your iPhone contacts list likely has only the first/last name and phone number for each person, whereas the Facebook app is far richer in its implementation of the very same contacts list -- because the person on the other side has gone to the trouble of keeping their address, phone, picture, and the like all fresh and up to date[1].

So the FB Phone would be an enormous improvement in contacts management over what we currently have, and an FB Phone Directory would probably not be long in following[2].

Once people are using the FB Phone, you'd want to heavily push FB Credits as the payment solution for everything. I am sure that from a fraud protection standpoint, the identity signals that an FB account provides are highly desirable to Visa and Mastercard. FB could also just cut out the middleman and do payments directly with an FB Card, instantly accepted by 800+ million people worldwide and countless businesses. Sign up for FB.com and accept/receive payments. Use the social graph for authentication, where each node has an authenticity rank (based on its date of first signup, number of non-commercial posts, number of authentic friends, and the like). It's easy to set up a fake email address, but much harder to fake a realistic profile for years and get "real people" to friend you and interact with you.

Thus, a Facebook purchase or clone of something like WePay or Square would seem like a logical move. Embrace the shift towards mobile and own mobile payments by owning identity. Owning identity means a lower risk profile and higher profit margin than any competitor in payments.

[1] Not incidentally, the use of the FB Phone would ensure that people have even more of an incentive to keep their contact information up to date and searchable.

[2] This directory would be a huge product in its own right and the core of a real social search product, something more along the lines of findpeopleonplus.com than anything that's called itself "social search" to this point. The purpose of social search is to find a person, not a web page.

Facebook will never grow revenue to 10x (matching Google) by continuing to sell display advertising on its own site.

However, it knows so much about users and keeps them logged in, so it definitely has potential to serve highly targeted or viral campaigns everywhere else on the web and mobile apps, a much better version of adsense.

Secondly, it is involving itself deeply in to user's habits and eventually may make a big play in to e-commerce, getting a cut out of every transaction made by the user (while frictionlessly sharing the information, of course). Credits is just in its infancy.

Finally, its learning so much about user's habits on the web that it can do a better job than Google at search, and make a killing on search ads.

$100b a bargain, I'm not so sure. I'd be more inclined to describe it as a fair valuation.

This is the real reason Google is getting desperate about Google+, they are worried about FB launching its own hyper targeted ad network. Google has context and tons of advertisers, FB has context and deep demographics and quite a lot of advertisers.

I think it's more that Google wants in on that demographically targeted ad-game. Right now search ads and facebook display ads are really different beasts.

For instance, in my business Facebook ads are worthless. We depend on user intent "I'm looking for THIS" (in our case local service professionals). In search that intent is very clear, in Facebook way less so.

If I was selling lifestyle merchandise or advertising a consumer site, Facebook would be really attractive I'd think.

Both sides want a big piece of what the other has.

Ads on other websites is definitely lucrative business, but if you want to make a parallel to Google, adsense only makes up 28% of total revenue [1]. This makes me kind of skeptical that a similar system for Facebook would double or triple their revenue. It's definitely possible that the parallel is wrong though.

i agree the outlooks on facebook are pretty good under your points. I should point out that Facebook, specifically zuckerburg has not shown interest in search, and has even said he does not want it in the past. It is also incredibly difficult to build an effective search engine. Incredibly difficult.

Facebook already solved mobile with News Feed ads.

Today, the most effective FB ads are the ones that show up in the News Feed after your friends "Like" or take action on an ad or brand page. The ROI on these ads crushes that of traditional display ads (including those on the FB right-side margin) AND the targeting is still in its nascency.

The best part is that these ads transfer seamlessly to mobile or any future platform.

Isn't HATEOAS (REST) a great case for #1? If all the APIs get their state from Facebook they could inject a 2-3 seconds ad between every XX requests or YY interval. I dislike ads just like the next guy, but this IMO is better than intrusive hooks inside the content, much like TV.

mobile use can be leveraged out by call-to-action approach including deals. ROI for call-to-action s much greater then for display ads and also revenue from deals can be more significant then it is today

Facebook is horrible for any kind of direct sale, the ads I see are rarely trying to sell anything directly. More people are trying to build page followings, give something free with an up sale, are attempting to sell something that can be seen as making the customer money or selling services with big margins (wedding based services comes to mind).

Bingo. I'm actually a bit surprised more people don't understand why this is the case and anticipate it.

Search is the optimal context for presenting an ad -- you have the chance to make an impression to a person who is looking for information about something right at that moment. If you can get the right ads correlated to the search terms, you're handing the user a URL to information they're already looking for.

In most other situations, ads are noise -- they're a distraction from what the user really came there to pay attention to.

In the case of Facebook, it's the user's friends and interests. Which means your real goal with a FB campaign is to get people liking/following you. Buying comes later.

100% agree. Even for interests, search is better. Google has a decade of my search history and much of my browsing history (via analytics). Even conversion history - what have I bought? FB has much less insight into my interests because there have been far fewer opportunities to learn about me.

I've had pretty good conversion from Facebook traffic, you do need to spend more time optimizing Facebook ads to get high converting traffic though. You'd expect Google to convert better than FB because presumably the google keyword search were transactional as opposed to passive traffic, but not at that ratio.

Were you doing multi-channel tracking ? - it's much more important when you're going after passive traffic sources in general.

My limited experience has been almost exactly the opposite of that. I think my conversion rate from FB has been significantly better because my software is niche and it's been easier for me to target on FB. But my Google Keyword-Fu could use some work, I'm sure.

Still, by far the best conversion comes from direct interaction with my community of potential users.

Out of curiosity, do you think this is because Google users were searching for something like your products, and FB users weren't? Or do you think it was something else?

Yes. No amount of demographic targeting will do you any good if there was no shopping intent. At least for apparel & other goods that don't offer immediate gratification.

Also out of curiousity, did your 200k come from facebook ads or from your facebook community (fanpage)? I would think that in the apparel business future engagement would be relevant, ie seasonal lines, sales, etc.

did you create the ads directly in the facebook interface?

FB traffic is not very good if you don't optimize and tweak your campaigns to find what works best, but 200k uniques and no conversions is insane and I'm sure you could make that work much, much better; and I have data to prove it

disclaimer: I work for one of the first fb ads API tool vendors, but I'm an engineer, not a salesperson :)

SAM ( http://www.brighteroption.com ); we were in the closed API program and have been running for about a year and a half now.

Don't let the marketing talk of the homepage fool you into thinking we are all social-mediay-businesslike, we run on smart code and awesome client servicing.

You forgot about fraud systems. Right now they only collect money -- once you start giving away money to websites who host Facebook ads, the incentive for fraud now exists. Google has done a lot of work in just securing the AdWords system from malicious gaming

Facebook actually has a big advantage there, in that it has a huge amount of personal data and verified phone numbers for it's users. It can use that data to prevent fraud.

They are doing a dual class offering. The class B shares (i.e. those held by Zuckerberg and other insiders) are going to have ten times the voting rights as the class A shares.

I wouldn't by into such an ownership structure, though to be fair, google has such a structure and those that bought that at IPO have done very well so far.

From the risks section:

As a result of voting agreements with certain stockholders, together with the shares he holds, Mark Zuckerberg, our founder, Chairman, and CEO, will be able to exercise voting rights with respect to an aggregate of XX shares of common stock, representing a majority of the voting power of our outstanding capital stock following our initial public offering. As a result, Mr. Zuckerberg has the ability to control the outcome of matters submitted to our stockholders for approval, including the election of directors and any merger, consolidation, or sale of all or substantially all of our assets. In addition, Mr. Zuckerberg has the ability to control the management and affairs of our company as a result of his position as our CEO and his ability to control the election of our directors. Additionally, in the event that Mr. Zuckerberg controls our company at the time of his death, control may be transferred to a person or entity that he designates as his successor. As a board member and officer, Mr. Zuckerberg owes a fiduciary duty to our stockholders and must act in good faith in a manner he reasonably believes to be in the best interests of our stockholders. As a stockholder, even a controlling stockholder, Mr. Zuckerberg is entitled to vote his shares, and shares over which he has voting control as a result of voting agreements, in his own interests, which may not always be in the interests of our stockholders generally.

> and must act in good faith in a manner he reasonably believes to be in the best interests of our stockholders. As a stockholder, even a controlling stockholder, Mr. Zuckerberg is entitled to vote his shares, and shares over which he has voting control as a result of voting agreements, in his own interests, which may not always be in the interests of our stockholders generally.

So he must act in good faith except when he doesn't. Got it.

No, he must act in good faith when acting in his capacity as a board member and corporate officer. When acting in his capacity as a shareholder, he has no such obligation. The line between the two roles is usually pretty clear.

Think of a member of a military. They have a clear duty to act according to the policy and orders of their superiors. But in most nations, they can also vote, in their personal capacity as citizens, to change the top level of leadership, and they have no obligation to exercise their vote in furtherance of anyone's agenda but their own.

Zuckerberg's position is similar. What's out of whack is that he controls a majority vote of the "citizenry" (shareholders) himself.

I don't know a lot about stock, so if you could explain to me how this works I'd be very thankful. Facebook is worth something like $100 billion, but their IPO is only for $5 billion. Doesn't that mean 95% of the company is still owned by... Facebook? (??) What fraction of the company are they selling by having a $5b IPO?

$5 billion is the value of the new shares that are being issued as part of the ipo. The valuation is expected to be between 75 and 100 billion, so essentially that means FB is selling between 5 and 6.6 percent of the company to raise the $5 billion. In that sense, it works exactly the same way that a new round of funding works from a VC. It doesn't however, mean that 95% of the company is owned by "facebook" since those shares can (presumably after some lockup period) be traded publicly. A lot of employees and investors, for example, will probably unload some of their shares on the public market.

I'm interested to hear why you wouldn't buy into that structure - is it a concern w/ Zuckerberg himself or an aversion to any situation where a single entity has majority voting rights?

Share ownership without votes is participation but not real ownership. In the long run companies can end up not being run in the interests of the shareholders. Most companies with these structures are valued at less than they would be with a normal structure. Classic example is News Corp where the Murdochs keep control with a minority ownership and run it much like a private company.

A public company should be public not half private.

I would under some circumstances, but there are absolutely no circumstances under which I would be prepared to invest in a company where one person has majority voting power. At least with Google, no single person's psychotic break can bring down the company.

One of the interesting gems in this filing is at the very end, it details stock grants for acquisitions so you can infer the running rate of talent acquisitions. So for example, "On February 28, 2011, we issued 681,357 shares of our Class A common stock as consideration to a company in connection with our purchase of certain assets from the company." You can cross reference these with news and correlate approximate acquisition cost based on the estimate value of price per share assuming, say, a valuation of $100 billion. So I'm guessing that the company I mentioned is Octazen and assuming a $100 billion valuation (~$50 per share), this comes out to about $35 million (assuming an entirely stock acquisition - note that Facebook spent, for example, $20 million aggregate in cash on acquisitions in 2010).

A small tidbit. FB paid Zuck $783,529 (3) in "other" compensation from his base 500k salary.

(3) The fine print.... The amount reported represent approximately $692,679 for costs related to personal use of aircraft chartered in connection with his comprehensive security program and on which family and friends flew during 2011.

One should also remember that in the infinite wisdom of the Congress and whoever was President at the time, any cash salary over $1 million gets an extra tax on top of normal income taxes. Better to pay for his security in before tax dollars.

It turns out that Zynga only accounts for 12% of their revenue.

"In 2011, Zynga accounted for approximately 12% of our revenue, which amount was comprised of revenue derived from payments processing fees related to Zynga’s sales of virtual goods and from direct advertising purchased by Zynga. Additionally, Zynga’s apps generate a significant number of pages on which we display ads from other advertisers."

It appears they would still be profitable without Zynga.

85% of revenue is from advertising. So either Zynga controls 80% of all non advertising revenue (aka the remaining 15%) or that 12% figure includes advertisements served on Zynga pages.

Is it reasonable to conclude that Zynga constitutes 80% of FB's credit ecosystem?

No, the 12% includes advertisements Zynga buys from Facebook, but not ads that appear on their pages.

"In 2011, Zynga accounted for approximately 12% of our revenue, which amount was comprised of revenue derived from payments processing fees related to Zynga’s sales of virtual goods and from direct advertising purchased by Zynga. Additionally, Zynga’s apps generate a significant number of pages on which we display ads from other advertisers."

Sadly the answer is yes (it is reasonable to assume 80% of FB's credit ecosystem targets Zynga assets). Check out Zynga's S-1 (since, thanks to the deal, most of zynga's revenue comes through FB credits, and those numbers will have been discounted because of FB's cut)

Facebook does not take a cut of third-party display advertising.

For example, if an advertiser pays Zynga to put a banner ad in their application or above the Flash widget containing their game, Facebook doesn't see a penny of that.

Zynga pays Facebook to advertiser in the right-hand column, though. Lots.

Additionally (and this doesn't count towards advertising revenue), Facebook Credits are mandatory for all games on the Facebook Platform, and Facebook takes a 30% cut any time a player purchases some.

"It appears they would still be profitable without Zynga."

That assumes many of those Zynga users would still be on, or use Facebook as often, if it wasn't for Zynga or other games on the platform. The significant amounts of time spent on Facebook is due in large part to games and photos. That length of time on the platform helps to drive display ad revenue.

Indeed it's curious why zynga never launched it. What's more, they no longer create standalone websites for their games like farmville.com. Maybe something having to do with that Facebook agreement?

<Interesting/> "Mobile" appears as risk factor in 2 instances.

- Growth in use of Facebook through our mobile products, where we do not currently display ads, as a substitute for use on personal computers may negatively affect our revenue and financial results;

- Facebook user growth and engagement on mobile devices depend upon effective operation with mobile operating systems, networks, and standards that we do not control;

They will be able to exert any control they want on the Windows Phone through Microsoft. Also, what prevents them from showing ads in mobile apps? They did a great work locking everyone out of functionality that would enable direct FB access, app developers can only access FB as an FB app, so no ad-less competition there.

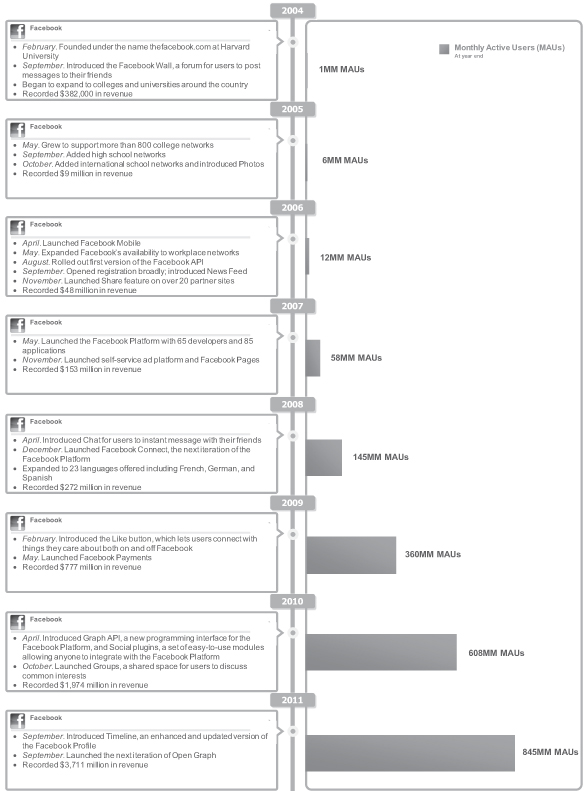

I'm curious as to what facebook did to generate $382k of revenue in 2004. Seems like a great start for a company of their size at the time. IIRC, they didn't turn on ads for a while afterwards.

Not sure about 2004 but I bought an ad on facebook in 2005. It was for a specific university and that was about the extent of the targeting if I remember correctly...

It looks like the accountant put in the perfect round figure of 1000 million for 2011 Net Income& then backed out all the other entries :) I used to do exactly that in my Accountancy 101 exams - Q.write the income statement for Acme Corp. What do you want Net Income to be ? XXX $. That means, TCO must be XXX - yyy, R&D must be XXX - zzz, and similarly back out everything else. Not saying they actually did that, just that seeing such perfectly round numbers reminded me of those exam problems.

Key information on revenue is on page 50. 85% of revenue comes from ads, which grew 69% Y/Y mostly driven by user growth (39% Y/Y) and showing a bunch more ads starting Q4 2010:

2011 Compared to 2010.

Revenue in 2011 increased $1,737 million, or 88% compared to 2010. The increase was due primarily to a 69% increase in advertising revenue to $3,154 million. Advertising revenue grew due to a 42% increase in thenumber of ads delivered and an 18% increase in the average price per ad delivered. The increase in ads delivered was driven primarily by user growth. The number of ads delivered was also affected by many other factors including product changes that significantly increased the number of ads on many Facebook pages beginning in the fourth quarter of 2010, partially offset byan increase in usage of our mobile products, where we do not show ads, and by various product changes implemented in 2011that in aggregate modestly reduced the number of ads on certain pages. The increase in average price per ad delivered was affected by factors including improvements in our ability to deliver more relevant ads to users and product changes that contributed to higher user interaction with the ads by increasing their relative prominence.

The key information is on page 54-55: Why the massive jump in Q4 2011 revenue over Q3? It looks like there is a seasonality factor, but their explanation only covers Q4 2010, to Q4 2011.

This is going to be a super volatile stock. If there Q1 2012 revenue is flat QoQ, this is probably a $50B company, if it is up 15%, then this is probably a $100B company.

The key information is on page 54-55: Why the massive jump in Q4 2011 revenue over Q3? It looks like there is a seasonality factor, but their explanation only covers Q4 2010, to Q4 2011.

This is going to be a super volatile stock. If the Q1 2012 revenue is flat QoQ, this is probably a $50B company, if it is up 15%, then this is probably a $100B company.

I was actually most curious to see if they had developed a source of revenue other than ads. It seems like the answer to that is mostly no, although they are working on payments.

I agree that ads revenue growth will be key for them in the short term. The Q4 2011 vs 2010 growth was 44% and it seems like perhaps the growth rate is slowing down.

Given that Google has made a ton of huge bets but doesn't make a dime outside of advertising, it is hard to think Facebook will move the needle with an alternative revenue stream. Even if they hit a Groupon sized home run with an alternative revenue stream, it only moves the valuation by 10-20%.

I think on balance mobile is not really an opportunity. They are losing the game revenue to the mobile/tablet platforms and in-app mobile monetization is a minimal opportunity for a task based application.

I don't use facebook, but can you explain what it means to be working on payments? I thought that was just their taking a 30% cut on game payments on their platform. That kind of margin doesn't exist for more general "payments".

Even with all my negativity, I am still cautiously bullish on Facebook. They are only making 50 cents/month per active user. I see no reason they can't double that.

You might not necessarily agree with the extent the word "hacker" is applied to nowadays, but considering you are in a site called "hacker news" you probably should

That's not a list of top shareholders (despite the headline). I think they only need to report the holdings of officers, directors, and anyone with more than 5%. Sean Parker does not fall into any of those categories, so they don't report his ownership.

While I don't know the specifics, it is very common for insiders to sell shares to new investors during later rounds. If I remember correctly, most of last year's goldman deal was from existing shareholders and not the company itself. So there is also a lot of opportunity to unload shares without using the formal markets as long as management is cooperative.

> it is very common for insiders to sell shares to new investors during later rounds.

Since when? Way back in the dark ages (2003), it was seen as a lack of faith in the company if the insiders were selling.

It is the paradox of the sale: If you think the stock is about to double or triple, why would you part with any of it? Sensible folks would go get a loan, esp with interest rates so low.

The idea is that by letting founders sell some of their stock early, investors and founders will be aligned and founders will be less likely to want or demand an earlier, safer exit that doesn't meet their investors' expectations. Basically, it lets founders get a few hundred K now so that they're more willing to try to go for broke later.

Founders Fund have even branded a share structure which allows easier conversion of co-founder (sometimes actually called Series FF) shares to shares of a later series sellable to investors in future rounds. I think that trying to grant early liquidity to founders has been common for at least two years and was a cause of major controversy during the Groupon IPO.

Since SOX? A perspective I've heard echoed by a few venture firms is that allowing insiders to sell a portion of the shares allows a bit of the pressure to come off and lets them focus on longer term value instead of wanting to rush into a liquidity event. Could be BS, who knows, but it's certainly happening.

A bird in the hand is still worth two in the bush, even if you're pretty sure you can get the two (or four) in the bush later.

Having been involved in a few startups where my equity was eventually valued at nothing, I'd certainly jump at the chance to sell some percentage of a future company I was involved with for real cash money even if I was pretty certain the stock might be worth more later.

Facebook's revenue will eventually shift from display advertising to data selling. There will come a time when no display campaign will run without input from Facebook.

Before any impression on any online media, advertisers will make a query to Facebook to find out which of the ads should be shown to this user. And Facebook will charge a small fee for each such query.

Interestingly, Google 2011 revenues are $37b, profits $9.7b, ratio almost exactly the same. Google also has 10x the number of employees as FB. Of course FB growth is much faster.

Consider that in 1996, there were far fewer people on the internet/web. It doesn't really make sense to compare absolute revenue numbers. Growth rates and revenue per user would probably be more interesting.

We're the 7 years of Google vs Facebook, comparing the growth from launch to IPO. Even in 2003, the amount of people and time spent online was far less than it is in 2012.

For example, there are an estimated 2 billion people online today, compared to 360 million in 2000.

Interesting salary history: 100% raise over 2 years.

Molly Graham, the daughter of Donald E. Graham, a member of our board of directors, is employed by us. During 2009, 2010, and 2011, Ms. Graham had total cash compensation, including base salary, bonus and other compensation, of $98,058, $133,620, and $189,168.

If you take a simplistic view of it, without assigning value to each person, doubling a person's salary is, while doubling profits, giving a raise that fits the success of the company, not a raise that says she played more or less than an average role within the company.

If you are logged on Facebook, never go on the website but still see the like-button that are scattered all around the web, do you count as an "monthly active user" ?

"We define a monthly active user as a registered Facebook user who logged in and visited Facebook through our website or a mobile device, or took an action to share content or activity with his or her Facebook friends or connections via a third-party website that is integrated with Facebook."

$1 Billion in profit => $1/(user year) in profit for 2011, correct?

That's pretty darn good money, but not a huge amount more room for user-growth. They'll grow by having new businesses/making current ones more profitable. New business would have to be monetizable (eventually, at least), current businesses would either have to convert better or become less costly to run.

Facebook is full of some smart cookies - it'll be interesting to see how they accomplish those paths.

I was thinking the same thing. Considering they have ~42% of all users (assuming the billion internet user estimate) there is only so much growth available from relying on their current model of acquiring users and serving ads to them.

I would imagine a next logical step would be to expand its ad network beyond facebook (i.e. serve facebook ads outside of facebook itself), it would allow for a significant jump in growth potential while staying close to their core competency.

As someone that lives in EU (as in, not in USA) and has no clue about stock market: what would be the easiest way for me to get a couple of hundred € worth of stocks in FB? Is that even possible?

You need to buy them on the day they IPO. You will not be able to buy it at the IPO price but at the price of the first minute of trading.

On top of that, "a couple of hundred €" is probably not enough money. The fees to buy stocks on the Nasdaq is usually in the tens of euro. You'll probably have between 10 and 50 euros of fees at the cheaper online trading platforms.

You can also call your traditional bank to buy the stocks but the fees would probably be higher.

You're not going to get in on the IPO price. That's for the banks who are selling to their very top-tier clients before it even starts trading on the exchange, basically.

Look into what is involved in buying stock in any American company from the EU. If you're still interested, you can pick up a few shares after it's trading on the exchanges.

Probably not, no. Most IPO shares are sold to large clients of brokerages. One of the inducements that large investment banks offer independent brokerages who use their services is letting them offer hot IPO stocks to some of their major customers.

Probably best to find a local broker that is on nasdaq. In the Netherlands, I would advise Binck or something similar. I personally have my companies stock in eTrade, but that is because that is how I received it :)

It can be tricky to get into the IPO though. Don't know the details on those rules.

I also don't really have a clue, but I think if you have a "trading depot" with some bank, they will offer you several stock exchanges to trade on. So you could pick some US stock exchange and buy the shares there.

- Using multiples is not a perfect method to understand the valuation of a business. It's one of many. It's a proxy. It's quick.

- This chart uses 2011 financial data. Facebook is growing fast - their multiples would come down significantly if we used 2012 projections - which we don't have. If I had more than 10 minutes on this - I would use 2nd half of 2011 or Q4 2011 as a run rate.

Quick Thoughts (Not Conclusions):

- In Ben Horowitz's argument against the bubble - he says the valuations they were seeing at AH for large private tech companies (like facebook) is in line with large public tech companies (google). So just looking at the data quickly, I was disappointed that FB appeared to have higher multiples (his blog post: http://bhorowitz.com/2011/03/24/bubble-trouble-i-don%E2%80%9...)

All of those numbers will be preliminary, they won't actually decide on number of shares offered and offering price (which determines their claimed valuation) until just before the offering. It depends on market conditions and what the large institutions say they're willing to pay.

"In the first quarter of 2012, our compensation committee discussed and approved a request by our CEO to reduce his base salary to $1 per year, effective January 1, 2013."

All of your compensation is in stock and worth the stock price.

1) It looks good to investors: you've got to believe in it if your worth is in the stock, for instance most of Bill Gates net worth is in Microsoft stock and it would look bad if he sold it all,

2) You pay lower taxes: capital gains vs income, not to mention

3) it sounds good in the press and when people say it

I had it explained to me that they have to take a salary to be eligible to receive company perks, such as a company car, travel expenses, etc. Therefore they take a nominal salary of $1 so that they are officially on the payroll and are receiving a salary, and hence can receive all the other perks and benefits through the company.

Probably to receive stock options in compensation. Sergey Brin, Larry Page and Eric Schmidt have also done the same. They seem to be exempt from payroll taxes in the United Sates.

Sometimes the explanation is more optimistic than that--sometimes the CEO is rich enough it makes little difference. E.g. John Mackey (Whole Foods CEO) switched to a $1 salary because he felt he no longer needed to work for money [1].

I mean, think about it: Mark owns over $10 billion in Facebook stock--he makes over a billion dollars by pushing the stock price up 10% (or loses over a billion if the stock drops 10%). Either way, a $15 million salary would be fairly insignificant...

Well, they're still taking a large salary, it's just in different currency. If you pay someone 1m dollars, 750k euros, or $1m worth of stock, it's still essentially salary...

I really wish everyone would stop talking about mobile access like it's this entirely new thing that's never been done before. Using facebook from a mobile device is absolutely, 100%, without room for debate using "the web". Sure it's a mobile device, but it's still HTTP and it's still a mobile browser based app. Just because it's not a "desktop" version of a browser does not mean the access isn't "web".

The issue with mobile is the limited screen real estate and the impact that has on being able to place ads. The mobile environment is different from the desktop environment, so it makes sense to distinguish the two. But you're right, calling the later "web" is a misnomer.

I agree with what people say about a Facebook phone. They might offer a smartphone for a heavily subsidized price and/or a feature phone for free. They might even offer free unlimited data, the catch for either model (and the data) is the that you log in with Facebook first thing, and maybe they'll restrict you to using only Facebook services, like messenger.

The site is really slow for me, maybe it's getting overloaded or ... something else. Either way, could someone post a summary of the filing? If I remember correctly there should be some pretty interesting figures; revenue, profit and so on.

I wonder how many employees are going to ditch the company after it goes public. They might have stuck around just for the IPO so they can hit big, take the money, leave, and start their own companies.

They won't be able to exercise their vested options for several months (usually six, as I recall). And many won't have vested 100% yet. That keeps people around.

3.711B in revenue and 3,200 employees at the end of 2011. That puts their revenue/employee numbers only slightly lower than Apple & Google, but beats Amazon. Impressive.

Reading this document makes me think Facebook don't know what's happening inside their own company. Facebook from all behavioural indications have been focused on maximizing short-term spend per advertiser rather than the long term revenue per user. Yet that doesn't seem to be reflected at all in their filing.

If you disagree with this statement I'd suggest you comment explaining why rather than just down-voting. Speaking as someone who bought over 35 million ads on Facebook last year, it's pretty evident that there's a mismatch between what Facebook are doing in practice and their view of what they're doing as portrayed by their SEC filing.

Rather than complaining about down-votes -- it would be awesome for you (who having bought a ton of FB ads knows that market really really well) to explain and justify your statement. Can you give us some examples of their short-term thinking?

It's pretty well known in the industry, for example they've long ignored requests for basic features (day-parting, A/B testing) that would improve conversion rates for advertisers because they would result in a short-term drop in advertiser spending even though making Facebook an effective advertising platform would be a better long-term solution (revenue wise).

edit: downvoter ... I just wanted to provide context for others so they wouldn't wonder what this is all about. I agree that this comment (parent) does not belong here ...

{kind=link}

{kind=link}

{kind=link}

IMO, Facebook's future depends on two things:

1) Figuring out how to serve up contextually relevant ads on mobile platforms in a nonintrusive and, ideally, useful way.

2) Figuring out how to serve up contextually relevant ads outside of Facebook, to Facebook Connect-backended partner sites and apps. (Sort of like an AdSense/AdWords hybrid, but based on very intelligent user-interest and browsing data).

I'm betting on #2's being the runaway breadwinner for Facebook in the long run. The longterm strategy seems to be to reduce reliance/dependence on Facebook.com in favor of Facebook Connect.