"When a measure becomes a target, it ceases to be a good measure."

The idea behind prices in a market economy is that they're an information-carrying abstraction. They let producers at every stage of the value chain understand the relative costs that go into different alternate ways of producing a good, without needing to understand every single stage of the supply chain and all the decisions that their suppliers made. And it also gives them information about relative demand, so that producers which make things that nobody want go bankrupt and those make things that lots of people want rake in windfall prices.

The whole point of the Fed is to alter prices, on one hand to keep producers from raking in windfall prices (price stability) and on the other to prevent too many of them from going bankrupt all at once (full unemployment).

Problem is that when you do this too much, for too long, the biggest input to a firm's production decisions becomes the Fed funds rate. When it goes up, time to layoff people, because the cost of capital just went up and you can't do anything without capital. When it goes down, time to go on a hiring frenzy because if there's money for the taking and you're not the one taking it, you get outcompeted by the ones who are. Over time this begins to dominate all other signals that pricing normally provides, like producing goods efficiently and making things lots of people want. You get companies like Uber, which lose money on every transaction but make it up in fundraising.

In turn this increases sensitivity to the Fed's actions, which limits their freedom to take them. If the whole economy breaks when you raise rates to 1.5% (as happened in 2019), it becomes very hard to raise rates above 1.5%. So rates get pegged below the natural rate of interest (which equilibrates supply of savings with demand for productive investment), lots of economically dubious projects get funded, you inflate a perma-bubble, and you can't deflate it without taking down the whole economy.

> The idea behind prices in a market economy is that they're an information-carrying abstraction.

No, the idea behind prices is that they are what the participants in particular trades think it is worth trading at.

The normative argument for the superiority of laissez-faire economies may involve market prices as an information carrying mechanism, but that normative argument is much newer than market economies, and is not the “idea behind prices in a market economy”. The benefits some people see (or imagine) in something after the fact are not the underlying purpose of the thing.

They aren’t. They are different, and one is actually the “idea behind prices in a market economy”, and the other is an academic argument, observing the fact of price setting in a market economy, for why price setting in a market economy is valuable to others besides the direct participants in the individual exchanges.

> Aren’t they, in fact, mutually dependent?

No, there is a one-way dependency between them. The normative argument depends on the fact, but not vice-versa.

> So rates get pegged below the natural rate of interest (which equilibrates supply of savings with demand for productive investment)

But the only body even attempting to determine what "productive investment" is and respond to it is the Fed. Savers are interested in money returns or at least preserving their holding which in many feasible circumstances (chronic instability, zero sum economies with fixed currency supply) is most reliably achieved by not investing in anything productive, not whether their investment makes optimal use of a country's productive capacity. There's nothing more "natural" about production decisions taking the spot price of a commodity the monetary authority has designated as money, or an arbitrary growth rate for money, or how badly undercapitalised wildcat banks are as inputs, and there's nothing about a regime not trying to avoid bubbles or busts that makes it inherently less likely to result in them.

But that's not true: every individual household and business is trying to maximize their profits (or at least, those that aren't are replaced by those that are), reducing their expenditures and increasing their revenues. In the presence of a stable money supply and stable prices, the only way to do this is through innovation and better efficiency: you reduce the value of your inputs, or you increase the value of the outputs. In the presence of external variations in the cost of capital, it becomes more profitable to capture that external capital than it is to increase efficiency.

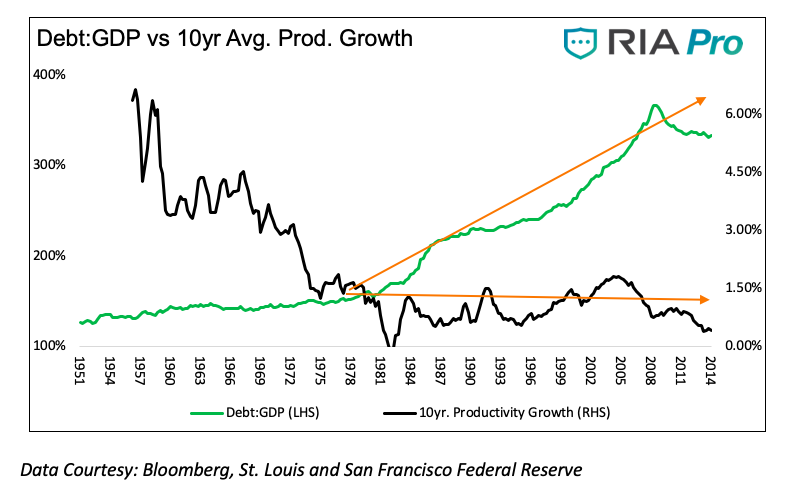

Peter Thiel and many other observers have noted that American innovativeness and productivity growth fell off a cliff c. 1971 [1]. He blames government regulation; however, a more likely explanation is that Nixon turned the U.S. dollar into a fully-fiat currency right around then, incentivizing people to compete for newly-created dollars rather than capture more of the ones circulating through the economy.

The causality might run the other way around too, as the Fed holds rates artificially low to paper over low real productivity growth, but this is not an improvement: it just means that we have a feedback loop between money-supply growth, inflation, and low real economic growth.

> In the presence of a stable money supply and stable prices, the only way to do this is through innovation and better efficiency: you reduce the value of your inputs, or you increase the value of the outputs

Or you decide the winning move is not to play, because borrowing is expensive, the purchasing power of your Benjamins won't diminish if you bury them in the ground, and investing money on capital goods in the hope of accumulating more money has negative average risk adjusted returns if there never is any more money in aggregate. On the other hand the way you capture the share of the growing pie is by increasing efficiency, it ceases to be an adequate investment strategy to just hold your capital in uninvested currency.

And taking a graph like that one where the sharp fall in productivity growth starts a couple of decades before leaving the gold standard and actually stops falling afterwards as evidence that leaving the gold standard caused productivity growth slowdown is peak gold bug dodgy graph interpretation! Bretton Woods collapsed because it was inherently unstable anyway.

My point is not so much that commodity money is stable as that fiat money is unstable. If you'd taken the opposite side of the debate I'd be happy to tell you everything that was wrong under the gold standard: frequent, severe, recessions; a tendency to hoard cash rather than investing it productively; lack of levers for governments to influence economic outcomes.

However, I posit that all of those downsides are inherently necessary to drive innovation and increase the efficiency of the economy. Bankruptcy and unemployment is how you garbage-collect inefficient ways of doing things: you want people to lose their jobs, because that forces them to take employment in more efficient sectors of the economy. Hoarding is how you a.) amass the capital stocks so that you can deploy them on bold opportunities when they arrive and b.) ensure that people are selective about which opportunities they pursue. If you encourage people to immediately invest any spare cash because the value of that cash goes down, you encourage them to seek out any marginal-productivity activity that might remotely be cash-flow, rather than waiting for big innovative opportunities that might take longer to appear.

In other words, I'm saying that there's no free lunch, a concept that should be familiar to any economist. You need failure to drive success. Mitigate failure and you also eliminate success. And the opportunity cost of suppressing serious failure for 50 years is stagnation, low productivity, and inflation, exactly what we've observed. All social systems eventually collapse; it's just that some people who remember how the previous social system collapsed become blind to how the current system is collapsing, because all they can do is think back to the problems it solved.

> the opportunity cost of suppressing serious failure for 50 years is stagnation, low productivity, and inflation, exactly what we've observed

But the United States is not the world, and the latter half of the twentieth century is not all of recorded history. The majority of the world grew further and faster over the period of modern money than at any other time in history (yes, there are other important reasons. There are other reasons why US productivity growth is not at its postwar peak too). The majority of recorded history on commodity standards, owners of wealth didn't patiently wait for the most innovative opportunities and direct resources better than the modern world, they hoarded, barely maintained their limited capital stock and much of the speculation that did take place was on capturing neighbours' hard assets rather than generating new wealth streams. US productivity growth in recent years might be below its postwar peak but is way ahead of historic norms, including the initial period of growth and labour saving device invention so unprecedented we call it the Industrial Revolution. Which doesn't mean the current system is ideal, it just means that everybody was worse off before.

Their argument is what the graph is actually showing is related to the fact that labour's share of US income peaked around 1970 and then began to drop, not some tautologically-defined concept of "production".

{kind=link}