Bogleheads is great, and one of the more wholesome things on the Web nowadays.

When my consulting business was finally doing well (after way too many years of school, debt, and turning down better-paying opportunities), it took me a few tries of asking around and Googling, to find what people were supposed to do with excess money. I ended up wasting some of it on naive sector investing, and on funds/stock-picking, before I stumbled upon Bogleheads.

Then I quickly settled into a simple your-age-in-bonds mix of ITOT and AGG (was already at Fidelity), and followed the Bogleheads advice of not touching it, not even looking at it. I also do the solo 401K, maxed contributions, and the HSA bonus (though the HSA was more headache than it was worth).

One of the odd things about Bogleheads, however, is that, once you're up to speed, have your accounts set up, no unusual events, and you take the "index on autopilot" to heart... frequenting the forum then seems counterproductive, like it becomes temptation to tinker with financial arrangements, or just a distraction from better things to be doing.

> One of the odd things about Bogleheads, however, is that, once you're up to speed, have your accounts set up, no unusual events, and you take the "index on autopilot" to heart... frequenting the forum then seems counterproductive, like it becomes temptation to tinker with financial arrangements, or just a distraction from better things to be doing.

That's what I've recently discovered. Dumping everything into VTSAX is the best thing you can do to your investments, but then... where's the excitement? So I've allowed myself a "fun money" brokerage account that I initially deposited $5k into, and just play with options trading. I've already paid myself back the initial investment, so any profit/loss from now on is irrelevant. This way I can still geek out over investing, but not gamble my life savings.

I do exactly this! VTSAX,VBTLX, and have a fun account.

My fun account has made me much more aware of global scientific news and research as I see my stocks jump up or level off; really neat understanding why.

Brokerages can front you the money to buy while your ACH transfer is being processed. Robinhood calls it Instant Deposits, but I believe others offer the service too for free.

What's the relationship here between EFI, mutual funds, and "margin account/higher expense ratio"? Would anyone be willing to explain this comment thread to a newbie?

In this thread, one person is saying they prefer MFs because they don't have to wait for an ACH transfer to complete, the other person is telling them to buy ETFs with a margin account (that is, using credit), because — as I interpret them — the cheaper ETF would be worth the interest on the margin.

But in this case, it's nonsensical if you're comparing VTSAX (0.04%/year expense ratio) and VTI (0.03%). If you have $10m in your account, the difference is $1k per year.

Often, ETFs have lower expense ratios because they are cheaper to manage; historically, mutual funds have had high fees, even for passively managed funds, and Vanguard is one of the companies that have worked to bring the fees down. But it's not always true that MFs are more expensive. VTSAX's ER is 0.04%; its ETF equivalent, VTI, is 0.03%. The difference is effectively zero.

I mean, many brokerages will extend margin for free during ACH transfer (or any settlement event for that matter). So using a margin account and buying the ETF will save you one basis point in fees every year. If you have a 30 year horizon it becomes ~20-30 basis points depending on contribution+return schedule. 20-30k on 10mm is not super much but not negligible either since it takes no effort.

TDAmeritrade will extend no interest margin for transfers iirc. I haven’t looked at robinhood in a while, but I believe they will extend instant deposit beyond $1k. I remember I had maybe 70k with them a year ago and my instant deposit was 50k. It still has to be no greater than max marginable value (so you can’t do it on a fresh account).

In Jason Zweig's commentary accompanying Benjamin Graham's book "The Intelligent Investor", he points out something similar:

> There are two ways to be an intelligent investor:

-by continually researching, selecting, and monitoring a dynamic mix of stocks, bonds, or mutual funds;

-or by creating a permanent portfolio that runs on autopilot and requires no further effort (but generates very little excitement).

> Graham calls the first approach "active" or "enterprising"; it takes lots of time and loads of energy. The "passive" or "defensive" strategy takes little time or effort but requires an almost scientific detachment from the alluring hullabaloo of the market. As the investment thinker Charles Ellis has explained, the enterprising approach is physically and intellectually taxing, while the defensive approach is emotionally demanding.

Later, Zweig goes on to say that if you must, restrict yourself to speculation with at most 10% of your assets.

> For better or worse, the gambling instinct is part of human nature--so it's futile for most people even to try suppressing it. But you must confine and restrain it. That's the single best way to make sure you will never fool yourself into confusing speculation with investment.

I suspect a lot of folks get tripped up during "the boring middle". It can be hard to resist the temptation to do something, anything.

I check my account balances and financial planning spreadsheet several times a week. But instead of mess with money, I try to channel that energy into modeling. "What would happen if I increase my savings rate by 5%? What if we took a year sabbatical?" Most of it goes nowhere, but I'd rather be futzing with a spreadsheet than gambling on Robinhood.

I've found the same thing. I joined the forum about a decade ago, and then went dark for several years. I'll go back to the forum whenever there are changes in my financial picture, or tax law changes. I highly appreciate the users on there with 10s of thousands of posts, always helping out the new people.

The moderators over there are excellent. Perhaps a bit overzealous at times, but probably better to err on the side of conserving the "wholesome" nature of the forum.

Tax law does occasionally change, and it can influence your most optimal financial path. For example, with the 2017 federal tax cuts capping SALT deductions at $10k, mortgage interest deduction went away for high-income earners in high-income states. The loss of a tax benefit makes home-ownership a slightly less attractive option.

In California, a single person pays $10k in state income tax on an income of about $142,510.

It's good to pay attention somewhat regularly, as it could impact planning. Annually, limits for 401(k)'s and IRA's are re-assessed, as well. When possible, you should take full advantage of completely filling tax-advantaged accounts (and not relying on last year's numbers).

I was active on the board back when it was on Morningstar. It helped me a lot, I contributed for a few years, and then I literally forgot about my investments for the next 15 years. Didn’t even look in 2008 and 2009. Highly recommended.

It only takes about 30 seconds to show that the BH site is anything but dogmatic. For example, check out the Hedgefundie thread on risk parity investing using leveraged ETFs (now at 9000 posts):

The bread and butter for BH is the unsophisticated investor who is paying their Edward Jones advisor 1-2% for an overly complicated, underperforming portfolio. These folks are better served by a simple plan (like the three fund portfolio) that they administer themselves. Their success in investing is mostly driven by advice to save and maintain long term exposure to the market. Saving that 1-2% makes a meaningful difference in their retirement lifestyle. Ordinary people can come with their portfolios and get free, unbiased financial advice that saves them thousands of dollars a year.

Investing discussions are the tip of the iceberg, though. Anything related to personal finance is germane. Discussions of tax planning, estate planning, withdrawal strategies, with participants who are experts in the field, are invaluable. For example, this long running thread with monthly posts that tracks a forward test of a mechanistic Variable Percentage Withdrawal strategy (as an alternative to the 4% rule):

Personal Consumer Issues section is golden for advice on purchases.

It's real secret, though, is the heavy moderation. It is very strongly curated around its subject matter, and in particular its "no politics" and "posts must be actionable" policies work to ensure that it has a very high signal-to-noise ratio.

> Saving that 1-2% makes a meaningful difference in their retirement lifestyle.

If you really want to see how much a few fractions of a percentage point can effect things a fellow named Larry Bates has a really good interactive page where you can enter various numbers:

I keep telling this to a friend of mine with a net worth in the single digit million $.

He pays (I think) 1.5%/year for a personal financial advisor, he says he's happy with it, but when I ask him what's the "alpha" [0] compared to, say, the S&P 500, he doesn't know. Ten years of huge growth in the stock market surely doesn't provide an incentive for him to investigate.

Investing style and method must match the temperament of the investor.

Your fried may not have the temperament that is suitable for managing investment decisions, even passively Bogglehead style. He may get better return by just paying 1.5% and staying completely ignorant and intentionally avoiding any knowledge. Paying 1.5% fee for the luxury of staying ignorant is still better than putting all money into inflation protected treasury bonds. Never try to push investment advice to your friends.

Paying an advisor doesn't solve the problem - how do you pick the advisor? That is actually a harder problem than implementing a three fund portfolio, and has even more emotional burden because successful advisors are good at making it emotionally difficult to quit.

A very good reason to pay an personal advisor is to structure your income, existing wealth, and businesses (et al) for optimal tax avoidance and tax-advantaged growth. These are fairly nuanced topics that are hard to do on your own, so it's possible that your friend is getting advice / action along those lines.

Obviously if it's 1.5% on AUM/year for stock picking advice, it's almost certainly not worth it. But you never know.

Other than perhaps tax-loss harvesting and muni bonds, my experience is that financial advisors know next to nothing about taxes. They aren’t accountants, and only know securities and derivatives and other basic investment vehicles.

They might have access to some exotic things that could be tax-advantaged, but again they aren’t accountants, and could care less what you pay on your gains.

In fact I would wager to say skillful accountants might have better investing advice for the rich than most any financial advisor.

> He pays (I think) 1.5%/year for a personal financial advisor

The financial part is solved nowadays with various low-fee funds. However, an advisor can still be useful for things tax accounting, estate planning, and general personal behavioural sanity checks.

So if he's paying that for the funds it is probably too much, but if it is for the services there may be some value there.

I found this Wikipedia-style page on personal finance advice for "managing a windfall" so well-written, that I was really startled (by the quality!). I came across it earlier today on HN in an "Ask HN" thread:

I had to help my Mom with personal finance. She is a first-generation immigrant who entered her late 60s with no stock or cash retirement savings, but with a lot of home equity value built up by sheer luck of buying a house in a booming suburb right before it really boomed, and holding it for 40 years. She lived paycheck-to-paycheck her whole life, and, because she fled communist Romania when she was in high school, she had a real distrust of the US financial system. (Perhaps warranted at times!)

So, I had to help her manage the windfall from the sale of her primary residence as she downsized her living space and needed to tap the newly-liquid cash as a kind of pension and healthcare issue rainy-day fund. She wanted to stick all the money under the mattress (quite literally).

I was in my mid-20s at the time (and a college-educated programmer, so savvy enough to wade through the systems), so I tried to wise up to the situation to help her out. I dealt with all the issues outlined in this page (on her behalf) via a lot of haphazard ad-hoc research and through expensive advice from personal lawyers and accountants.

I am impressed with the way in which the page tackles not just the pragmatic issues, but also the psychological ones -- e.g. that someone facing a windfall will feel temporarily "rich" because they are newly in the money, and thus won't manage smartly toward a long-term future, and may also be more prone to frivolous purchases.

Financial literacy is a really hard thing and so much of the information you find is biased and is selling you one thing or another.

I wish I had known about this page -- and the wiki overall -- years ago. The "Bogleheads" philosophy aligns a lot with my personal outlook, which has a a lot of trust for the power of markets and financial management, but a whole lot of distrust for financial advisors and money managers. Now that I've been on this side of the table, representing my Mom's interests in retirement, it became really clear to me why fraud against the elderly is so common, and why it's a very legitimate interest to ensure they are well-protected if they don't have savvy family members who can guide them through it.

I did something similar with my mom. After she got divorced, she ended up with a pile of money and no idea on what to do. I basically walked her through the a simple portfolio - equity/bond mix (30/70 as she was close to retirement), and a mix of domestic and international broad index funds.

She was able to go into her bank, setup a brokerage account, and basically tell them what she wanted. 20 years later, her money will outlast her. And it wasn't a ton of money to start with - if she had taken even a 20% loss, I would have worried if she'd have enough.

The Bogleheads site is fantastic. Both the wiki and the discussion board are of high quality; the board is one of those rare niche "Web 1.0" boards with super-knowledgeable posters that almost doesn't exist anymore.

The book (The Bogleheads' Guide to Imvesting), written by the website creators, is also one of the best introduction to passive investing. A must for anyone starting out needing to figure out the ins and outs of IRAs, ETFs etc.

Obviously these old Web 1.0 sites are still relevant because they ~always had high-quality content. I wonder if not jumping on the latest design bandwagon helped cement them in that place. And how much does the design turn off the average Robinhood investor (and I do mean investor, not speculator)?

For those who are new to boglehead history, John Bogle was the CEO of Vanguard and is credited with creating the first index fund. Maybe it's just the branding and history, but Vanguard is the only financial institute I think of as a friend.

The Vanguard ownership and revenue structure is very weird and the subject of multiple IRS and SEC private rulings. It’s not a mutualized organization like a mutual insurance company.

Each mutual fund is a separate corporation and contracts with a management company. This is standard across the industry. The Vanguard “twist” is that all Vanguard funds contract with the same central management company. Each fund also owns a share of this company. The management company charges the funds for its services at cost. This has been the subject of at least one lawsuit, alleging that Vanguard is engaging in anti-competitive behavior by not charging funds for management services at an arms length level.

The passive investment strategy was very good for me. I was quite active before, lost a lot of money, was occupied with the topic daily. Now I have peace of mind and a great return on my money.

The book that made me rethink everything is “The simple path to wealth” by JL Collins. It’s basically a round up of his blog posts. Although the title is a bit cheesy I can’t over recommend the blog/his book. It’s eye opening and straight forward to implement. He only recommends funds of Vanguard, John Bogle’s fund.

A lot of the stuff on the wiki and site is massively simplified and not strictly true. If you don't know much about finance, stuff like "return is always associated with risk, there is no free-lunch" is a good place to start, but more knowledgeable and quantitative investors know that this isn't true (according to CAPM, only systematic risk generates return, not specific risk).

If you haven't thought much about what kind of volatility you are okay with and aren't really interested in managing your money, a boglehead kind of portfolio is good place to start. It's something, for example, that I might recommend my mom, if I wasn't willing to put in the work to manage her investments for her.

But for a technical crowd, like HN, the stuff on the site misrepresents modern financial theory and perpetuates people saying stuff that doesn't even make any sense, like, "you can't beat the market", "don't hold a leveraged index fund", "active management is a scam", etc. Like all things people say, these have a kernel of truth, but the specifics and context are so far removed that these statements become meaningless, or even flat out wrong.

Even by just holding simple, automated ETFs (I don't call this passive investing, because passive investing doesn't exist), there's tons of room for really interesting optimizations that increase return and decrease risk. Things like risk parity portfolios, minimum variance optimizations, persistent factor portfolios, etc.

And best of all, with zero commissions, super tight bid-ask spreads, and easy to access APIs, "quant-lite" investing is more accessible than every before.

In conclusion, every portfolio is an active portfolio, from deciding a equity/bond ratio, to investing in real estate, to deciding to buy some TSLA. It's all the same, so stay away from any dogmatic approaches to investing (I would say the bogleheads are pretty dogmatic). By becoming familiar with the biggest and most important advances in quantitative finance, along with understanding your own risk tolerance, you can construct a portfolio that is perfect for you, and that will give you so much more than a one-size-fits-all boglehead portfolio could ever hope to.

I don’t know your background. But I’ve worked at an investment bank the past 15 years and have traded every kind of stock, bond and derivative there is.

With respect, you sound a little bit like every new programmer that I’ve worked with. They get a taste of learning about finance and suddenly become day traders. They make some money and then suddenly they give it all back and more because they really weren’t understanding what they were doing.

In general, anyone with a full time job that thinks they can out-compete full time traders that specialize in the exact instrument that you are trying to trade will have a very expensive lesson some day.

If you really want to pursue it at least take the level 1 CFA exam. If you can’t pass that you don’t have much of a chance and if you can pass that you’ll probably realize you don’t want to do it.

Could someone with your experience help me on where to get started if I want an in depth knowledge of the kind of stuff you use on a day to day basis? Would preparing for and writing the level 1 CFA be a good start? (I'm a mathematical physics graduate who's done quite a bit of software in finance but not specifically in trading).

I've read quite a bit of quant material, but I would also like to know what to learn from someone who is steeped in the industry as I'm sure my knowledge is quite a rough approximation of what I should actually know if I were to claim any expertise.

CFA Level 1 official prep material is very good. IIRC, these are set of 6 books. You can get second hand older prep material from eBay/Craigslist/FB for cheap.

> “ In general, anyone with a full time job that thinks they can out-compete full time traders that specialize in the exact instrument that you are trying to trade will have a very expensive lesson some day.”

I hear this a lot and it’s definitely something I would expect to be true. But I’ve been repeatedly surprised that it’s not.

I’ve made a lot investing on the side (usually just stock, sometimes calls - recently for peloton in January, stock for tesla in 2012 which I sold early last year before the crazy recent rise, stock for Apple, Amazon, Nvidia, Facebook, AMD).

Am I stupid, lucky or both?

Yes longest bull run in history, but investing in large tech companies you think are stable long term with good CEOs when you know the field (Apple, Amazon) seems pretty easy.

When you read a lot of comments from traders on the east coast they seem like they misunderstand the companies, or are not focused on long term strategic moves.

I’m mostly positioned in total market index funds with a couple large positions in companies I think will continue to outperform long term, but it doesn’t seem that hard to do better than traders.

Plus the index funds contain a lot of companies I would never personally invest in if they weren’t in the fund, still good to hedge against my own (likely) arrogance.

I did sell each of them after while (once I got long term capital gains and needed the money for something else or wanted to move to a different stock).

So day traders no, but other traders yes? Particularly the peloton calls (2yr expiration leaps) were an explicit trade against some industry person that was extremely wrong.

I used to work in finance doing portfolio analytics. I'm not really advocating day trading, but rather using quantitative methods for optimal portfolio construction.

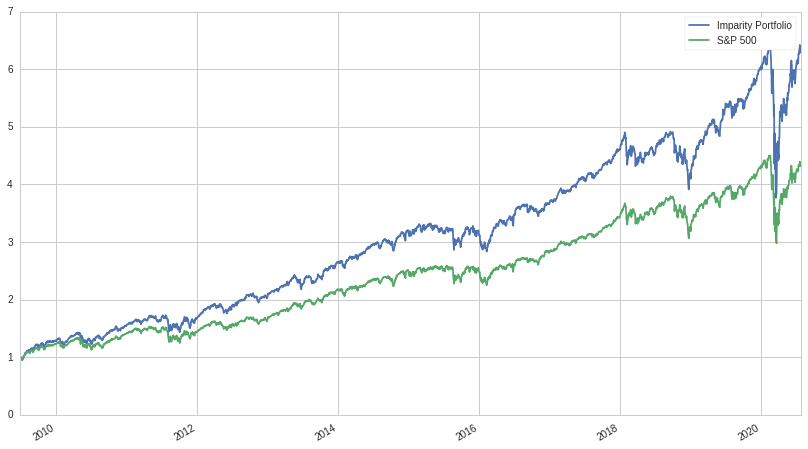

>For example, if we purchased a 2x bull leveraged S&P 500 ETF such as SSO, we would choose an appropriate weight to cancel out the leverage, 0.5 in this case. If we kept the rest of the money in cash, the return of the portfolio would only be slightly worse than that of the S&P 500, due to the 0.90% expense ratio we pay.

A 2x bull leveraged etf replicates daily moves. your long term return to expense expectations are completely off.

You are exactly correct. So many people are buying these synthetic instruments without even reading the prospectus that clearly states in plain language what you said but they still buy them expecting > daily tracking.

I’ve seen so many strategies that technology people come up with (including myself) that look great on paper but don’t take into account the prospectus or things like market conditions, counterparty risk, backwardation, contango, etc.

You're right that 0.9% is a lot, but the expenses get absorbed by the bond yield. The total difference of return between 0.5*SSO and SPY over the ten year period (2010-01-01 and 2020-01-01) is 28%. Maybe you're right that that's more than "slightly" worse, I'll change the wording.

Moreover, when doing at the historical returns, I do use UPRO, not just 3xSPY, so the expense ratio is included. It's not included in the chart that goes back to 2004, but I do mention that that one is synthetic and inaccurate.

Its not labeled on the axis. But the analysis is up to last Friday. It's also easy to see that the huge drop and rebound at the end of Coronavirus. The start and end date are also mentioned in the post.

> return is always associated with risk ... this isn't true ... only systematic risk generates return

On the contrary, your criticism that "only systematic risk generates return" does not invalidate the assertion that "return is always associated with risk". Perhaps you misinterpreted the direction of causality implied by that assertion, thinking that it meant risk is always associated with return?

You can take on more risk and not get any more return. Conversely, you can get more return and not take on anymore risk. That's like the foundation of Modern Portfolio Theory.

Theory tells us that you can't get more return without taking on more risk, if the market is efficient.

Of course, the market can't be perfectly efficient, but it's possible that the market is weakly efficient: the cost of information is so high that it, on average, makes it impossible to beat the market.

No, only if the portfolio is on the efficient frontier. There are many sub-optimal portfolios that do not have the best return/risk trade-off, like portfolios with a lot of specific risk. Check out the Markowitz Bullet.

Specific risk does not get compensated because it is easy to eliminate it with diversification.

I should have been more specific (no pun intended). You should take a closer read of my comment. You've made the same misinterpretation a second time.

Suppose a non-diversified investor, A, owns an asset which has both systemic risk and specific risk, and a diversified investor, B, has the same knowledge as A. In this case, B would be willing to pay a higher price for the asset than A would. A then sells the asset to B and the market becomes efficient. No assets would exist not on the efficient frontier.

You can, but not consistently according to the Efficient Market Hypothesis. If you are referring to e.g. factor investing, that's not "beating the market" in the traditional fund manager way, just holding it differently and taking more systemic risk for a higher potential upside (if the factor is indeed based on risk and not irrationality of market participants).

> And best of all, with zero commissions, super tight bid-ask spreads, and easy to access APIs, "quant-lite" investing is more accessible than every before.

I'm conservative here and would wait 10 years before jumping on some fancy new technique to make more money. Why? Because fin history is littered with fancy new ways of making money that primarily made the manager money. Any real advantages are going to be quickly taken up by competing money makers anyway.

> In conclusion, every portfolio is an active portfolio, from deciding a equity/bond ratio, to investing in real estate, to deciding to buy some TSLA. It's all the same, so stay away from any dogmatic approaches to investing

This is dangerously wrong advice. "Passive investing" in the Bogleheads sense and choosing e.g. a equity/bond ratio is based on science and 120+ years of available data (Efficient Market Hypothesis, Modern Portfolio Theory), buying TSLA is not. Real estate is a very mixed bag (for US research, see e.g. Beracha et al. 2012 "Lessons from over 30 years of buy versus rent decisions" in Real Estate Economics Vol 40 No 2, and https://www.prnewswire.com/news-releases/house-of-cards-morn...).

Conclusion: the "dogmatic" approach is absolutely the right thing for 99% of retail investors to follow.

During the same time, bonds sold off too. Everything did.

If you were dollar cost averaging into the market for 12 years, you could find yourself below where you started. That's a pretty demoralizing situation.

I think being aware of market conditions and reallocating as you see fit is just part of being a responsible adult. Maybe sometimes you do want to hold VTI, but also it's not unreasonable to bet on Elon.

I'm not saying everyone has to be highly leveraged and aggressive, but I think you're putting a tremendous amount of faith in the markets and intentionally looking the other way.

This does not account for dividends, which, if reinvested, would have produced a 22% gain during this time period, which is not too bad when "everything was selling off"

Not spectacular, but you also need to compare this to whatever alternate investments you would have chosen at that time, and would have kept until now. Gold, Cash, small caps, real estate, multi-factor, managed futures, ?

You also need to consider why you have chosen these to points in time.

Looking backwards, there were probably better things to do with your money during that specific time period, but would you have chosen them in 1996 ? And would you have kept them until today ? And, if not, would the changes you would make have also done well ? You would need to be right in both investment selection and timing many times to have done better than the SP has done.

I wasn't accounting for reinvested dividends, but inflation from 1997 to 2009 was 34%.

I'm choosing those points because I remember hearing from retirees in 2008 that they had followed all of the advice and they are worse off than they were 10+ years ago. I saw too many cases of people being upside-down on their mortgages, while losing their jobs, while losing their retirements. In that situation, it's pretty hard to keep saying "don't worry, it'll come back, just keep dollar cost averaging in". If you were retiring in 2008, you might not be able to keep averaging with the market, even if you had the stomach to do it. Time in the market is still timing the market.

We've only had modern portfolio theory since 1952. In the last few decades, we've done some really experimental monetary policy. I won't be shocked if we experience some event that brings us back to 2008 levels. I also won't be shocked if we see hyperinflation. The one thing I know is that you're always trying to time the market, it's just a question of if you acknowledge it or not.

I think it's a good idea to max out your tax-advantaged retirement plans and dump them in indexes as sort of a safety net because your MPT advice is probably "too big to fail" at this point, but that only accounts for less than 20k/year of investment advice (for most employed people). After that, investing in a residence makes a lot of sense because of the tax advantages. If you happen to be in a situation where you can engineer more tax advantages (like owning a business or moving to a lower-tax state), then definitely do that. Once you've got all that sorted, it's pretty much just gambling.

> If you were retiring in 2008, you might not be able to keep averaging with the market, even if you had the stomach to do it.

That is why you need to risk-adjust your portfolio before you hit retirement and see to it that you have other assets to fall back on in case of market implosions. Landing in a ditch with your stocks as the only possible income during 2008 means your assessment of your risk tolerance was wrong and you found that out the hard way. Staying in stocks means accepting the risk that things go south in exchange for high potential returns. As we saw, the markets climbed back (I think the average is 2-3 years of misery in past crises before it gets back up) and had a 10-year bull run before Corona hit.

A fully paid off house can help sit out crashes, too, sure. Investing in stocks while still paying your house off, well... some people like to live on the edge :-)

> Time in the market is still timing the market.

No. Timing the market is making decisions in between about getting in and out for other things than rebalancing, adjusting your risk or for some rational tax purpose.

As mmmrk responded, you need to settle on a risk profile.It is not all or nothing.

You should assume the "market" will go down 50% at any given time, and ask yourself how that would effect you. You need how much to keep in "safe" assets, such as quality bonds and/or cash.

If you are retired and your assets drop in half, will you be ok ? If not, reduce equity exposure until you reach a point where you will be ok.

I aim to own my house outright, and have no more than 50% in equities. That's me, that's my risk tolerance. If the market goes down by 50%, I am still fine, from a financial perspective. So I would not feel the need to sell in a panic. If I had a large mortgage, all stock, I would probably panic.

Owning a business, imo, is much riskier. You can go out of business and also end up in debt. Imagine if you owned a bunch of restaurants right now.

Again, what is the alternative ? Managed futures, minimum volatilty, small cap, factors, oil rigs, private equity - none of these have shown to work when the st hits the fan. Maybe gold.

And on other dates, it was not $773. So what? Long term, the world market (more than the US) historically averaged to 6-8% growth p.a. with dividends before inflation iirc, and the last 120 years were certainly no walk in the park for the world. If you look at the MSCI World in the past 30 or 40 years, you would have made no loss in any time window if you bought and held at least 15 years. The key is time in the market. 12 years isn't much. Think 20, 30+ or until you die. Psychological pain in downturns is the price you pay for far superior returns in the long run to any other asset class.

Switching between VTI and single shares is market timing and therefore gambling. If you want to reduce the maximum drawdown, ramp up the allocation of less risky assets like bonds or cash on a savings account.

While I largely agree with your post, you are forgetting about the total return, yes the S&P was like for like on a net basis, but dont forget about dividends in the intermediate period.

there's obviously a lot of folks here who aren't "technical", see endless stream of "how to find a technical cofounder"-esque posts. (and that's ok!)

and even the engineering school and math grads floating around on here can't be expected to have significant financial expertise.

> If you haven't thought much about what kind of volatility you are okay with and aren't really interested in managing your money, a boglehead kind of portfolio is good place to start.

that's most people! even on HN!

> By becoming familiar with the biggest and most important advances in quantitative finance

i'd love to see a summary or jumping off point for this.

But the "you" here isn't you, it's people who aren't hobbyist investors (let alone professionals). People who don't know, and don't really want to know, what "risk parity" or "minimum variance" is. I don't think any boglehead truly believes nobody can beat the market.

> The Bogleheads® emphasize starting early, living below one's means, regular saving, broad diversification, simplicity, and sticking to one's investment plan regardless of market conditions.

I've heard about Bogleheads for the first time today. Twice! I thought it would be interesting for HN readers to know about it too.

With the demise of FatWallet Finance (which I read daily) I haven't really had a good source for the kind of content that used to live there.

The Bogleheads forums live in kind of a parallel universe, with sometimes very similar content but a very different outlook. I try to read weekly but a lot of it is kind of "interesting but not useful".

Another interesting resource, although not my niche, is the Whitecoatinvestor forums, which offer a neat view at a very specific profession's finances at every stage of their career.

Almost 50, after a few boom and bust years, I’m finally debt free, but have zero savings or retirement, and make north of $200K. I have a partner to think about in my plans (so, retirement for two).

Job will let me work from home permanently, so I’m moving to Nevada.

I can aim to max out 401k contributions, and then what? I consider things like side hustles (with my partner) that could generate additional incomes which would go straight to retirement. I considered investing in a B&M business that would generate modest income that could go to retirement but that’s a weird option given pandemic circumstances.

I may be generating more income at some point that would let me pivot to self employment with non-salaried caps on income, but I won’t know for about a year (side hustle generating money isn’t past that “it’ll be stable now” maturity level yet).

the bogleheads wiki and forum is of course, a great resource, better than HN for this.

> I can aim to max out 401k contributions, and then what?

unless your 401k has extremely good expense ratios (<0.1%), i'd: put enough into the 401k to get the full employer match, then max vanguard/fidelity/schwab IRAs for yourself and your partner. then go back and max the 401k.

(i think you'll want to do a backdoor roth on that IRA, but i'm not familiar with that, as my income isn't quite there yet.)

at 200k i expect you can pull all of that off easily enough.

> I consider things like side hustles...

at this point you're already generating more funds than you can squeeze into tax advantaged status. so... make as much as you can, save as much of it as you can, and aim towards investments that produce fewer dividends, so that you can reduce your tax burden.

Reminds me so starkly of how much of the Internet has moved into single websites like Reddit. I definitely enjoyed browsing a huge variety of interesting forums in the past, but the amount I go to nowadays is much smaller. Convenience is nice, but it still feels like something has been lost.

This forum is a treasure trove of financial information but it's too much for me to read. Hmmm.. if only a computer program can read all that and tell me what to do. Does GPT3's training set include this? I want it to be my financial advisor.

I like Bogleheads and their philosophy, but I do worry about the risks of advertising doing things on autopilot.

If index funds become big enough the equilibrium for active traders shifts from trying to own great companies to trying to game the index fund algorithm. Investors have to pay at least a little attention to the market to make sure that they are still sane.

Part of the funds' expenses (thus the expense ratio) are investment in techniques/technologies to avoid getting fleeced by hedge funds as they rebalance.

In the same category, if you live in the UK then http://monevator.com is the go to source for passive investing advice. The comments section is a gold mine as well.

Boglehead stuff is safe and easy. It’s too dogmatic for me in 2020. Following their advice Is good for a 401k, but means holding a lot of garbage. Owning the whole market was smart in 1990. We do not live in 1990.

My portfolio of 5-6 stocks + cash has beat any Boglehead portfolio, and has for decades now with a minimum investment in time. No bonds except for GNMA 15-20 years ago.

It’s not that hard. AAPL and AMZN have outperformed the market for 15-20 years.

>It’s not that hard. AAPL and AMZN have outperformed the market for 15-20 years

If you stuck with both of those for 20 years and didn't get distracted by anything else, good for you.

However, it's hard for me to believe someone who is old enough to be investing 20 years ago and followed their ups and downs would call it easy.

Most of what I've learned in my entire life about investing is from not putting everything I could in Apple stock and trying to think honestly about why that is.

It certainly wasn't obvious to me and I think most people circa 2000 that either AMZN or AAPL would become trillion dollar companies. Jobs and Bezos weren't considered gods yet. The dot-com crash meant that Amazon looked like another not-quite-dead-yet victim staggering around. Apple had yet to invent any of the things that make up most of its business now.

When Apple opened the iTunes store, in 2003, that's when I believed in them...briefly. But when they broke out of their historical range, I figured, that's it, and never imagined they would keep on going.

And after years of not believing in or liking Jobs, not liking OS X, etc., when he died, it made sense to me to assume Apple would collapse without him. After all, that's what happened the first time he left.

So it's easier for me to believe that someone who says it wasn't that hard to predict the last 20 years just is lying about living through it. But of course that's self serving of me - maybe you could explain how you kept the faith through everything that happened.

I would say that it's true that performance of a stock like Apple persists for many years, so it sounds wrong to say you can't predict it. But the trouble is, when you don't have the benefit of hindsight, you have to again predict it will continue every day of every year for all those years.

20 years ago AAPL was an absolute dog of a stock. It had underperformed the market for years. For the layperson AMZN was hard to distinguish from WebVan or pets.com.

Good on you for identifying their value at the time and getting rich, but it's not something everyone can do.

Yea Amazon was an easy bet back in the 90's clearly that bookshop would move into selling everything, optimizing warehousing and start the biggest cloud computing service. Oh hold on...

Sure it is. I’ve been investing in stocks and funds since high school in the early 90s with summer job money, and beat the indexes 22/25 years.

People buy and sell houses all of the time and find ways to make money. It’s no different with securities, and the bizarre position that responsible investing for individuals consists of being actively ignorant is gross.

Index investing is a valid, useful tool. It should not be a quasi-religion.

You make it sound simple, and you probably are a skilled investor. Again, good for you!

But you have to realize you're essentially saying "Why can't everyone be better than average?" It's great thing to aspire to but most people won't be better than average. Anyone can, everyone can't.

You can also easily see this in the reduced bargaining power of the bottom 3 to 4 quintiles of the American people, as evidenced by their stagnating or declining pay and higher volatility in the demand for their labor.

lol. “Don’t gamble! Take all your savings and buy some good stock and hold it till it goes up, then sell it. If it don’t go up, don’t buy it.” —Will Rogers

{kind=link}

When my consulting business was finally doing well (after way too many years of school, debt, and turning down better-paying opportunities), it took me a few tries of asking around and Googling, to find what people were supposed to do with excess money. I ended up wasting some of it on naive sector investing, and on funds/stock-picking, before I stumbled upon Bogleheads.

Then I quickly settled into a simple your-age-in-bonds mix of ITOT and AGG (was already at Fidelity), and followed the Bogleheads advice of not touching it, not even looking at it. I also do the solo 401K, maxed contributions, and the HSA bonus (though the HSA was more headache than it was worth).

One of the odd things about Bogleheads, however, is that, once you're up to speed, have your accounts set up, no unusual events, and you take the "index on autopilot" to heart... frequenting the forum then seems counterproductive, like it becomes temptation to tinker with financial arrangements, or just a distraction from better things to be doing.